In this post

Lorem ipsum dolor sit amet

Lorem ipsum dolor sit amet

Most HR leaders aren’t asking, “Should we offer more benefits?” They’re asking, “Why aren’t employees using the ones we already pay for?”

That gap between spend and actual impact is what’s driving the rise of lifestyle spending accounts (LSAs). They offer a flexible, employee-directed alternative to rigid, one-size-fits-all benefits. To that end, LSAs have grown significantly over the past several years—the Benepass 2026 Benchmarking Report shows an average utilization rate of 83%.

But flexibility comes with trade-offs. Before you commit budget and operational resources, it’s worth understanding how LSAs actually perform in practice. This guide breaks down the key pros and cons so you can decide whether an LSA fits your workforce, your budget, and your broader benefits strategy.

What are lifestyle spending accounts, and why do they matter?

A lifestyle spending account is an employer-funded benefit that gives employees a set annual or monthly allowance to spend across a defined range of lifestyle-related expense categories.

Unlike health savings accounts (HSAs) or flexible spending accounts (FSAs), LSAs aren't governed by IRS pre-tax rules, meaning employers have significant freedom in how they design them. You choose the eligible categories, set the allocation amount, and employees decide how to use their funds within those boundaries.

Common LSA spending categories include:

- Fitness and wellness

- Professional development

- Family care

- Mental health

- Food and nutrition

- Remote work expenses

Rather than negotiating separate vendor contracts for a gym membership subsidy, a learning stipend, and a childcare reimbursement program, you consolidate everything into one account structure.

This addresses a persistent challenge: how to deliver meaningful benefits to a multigenerational, geographically distributed workforce without adding administrative complexity. A remote employee in Austin has different priorities than an on-site parent in Chicago, and LSAs let both access support that actually fits their lives.

The rise of hybrid and remote work has further accelerated LSA adoption. When employees aren't sharing a physical office, location-specific perks lose their value. LSAs adapt naturally to distributed teams because employees direct their own spending rather than relying on employer-selected vendors or on-site amenities.

What are the key advantages of lifestyle spending accounts?

LSAs offer strategic advantages that go beyond simple perk distribution. When designed well, they drive measurable improvements in retention, administrative efficiency, and budget control.

Enhanced employee satisfaction and retention

By allowing employees to direct funds toward what matters most, you create a lifestyle benefits experience that feels personal rather than prescriptive.

This flexibility is especially valuable for multigenerational workforces: Gen Z may prioritize student loan support and mental health resources, while Gen X employees with aging parents may value elder care assistance. An LSA supports both without requiring separate vendors or multiple reimbursement processes.

When employees can use benefits that align with their life stage and priorities, they’re more likely to view their total compensation as competitive.

LSAs also help you reinforce company culture and values in a tangible way. For example:

- If you prioritize wellness, you can fund fitness and mental health categories.

- If you emphasize continuous learning, you can support professional development.

Over time, this alignment strengthens your employer brand with both current employees and candidates.

Flexible benefit design and administration

One of the most practical advantages of LSAs is consolidation. Instead of managing multiple stipend programs, you bring everything into a single account structure with spending categories. This shift reduces day-to-day administrative work for HR and finance teams with a few key benefits:

- Fewer vendor relationships to manage

- One source of reporting across all spending categories

- The ability to adjust allocations mid-year without renegotiating contracts or waiting for open enrollment

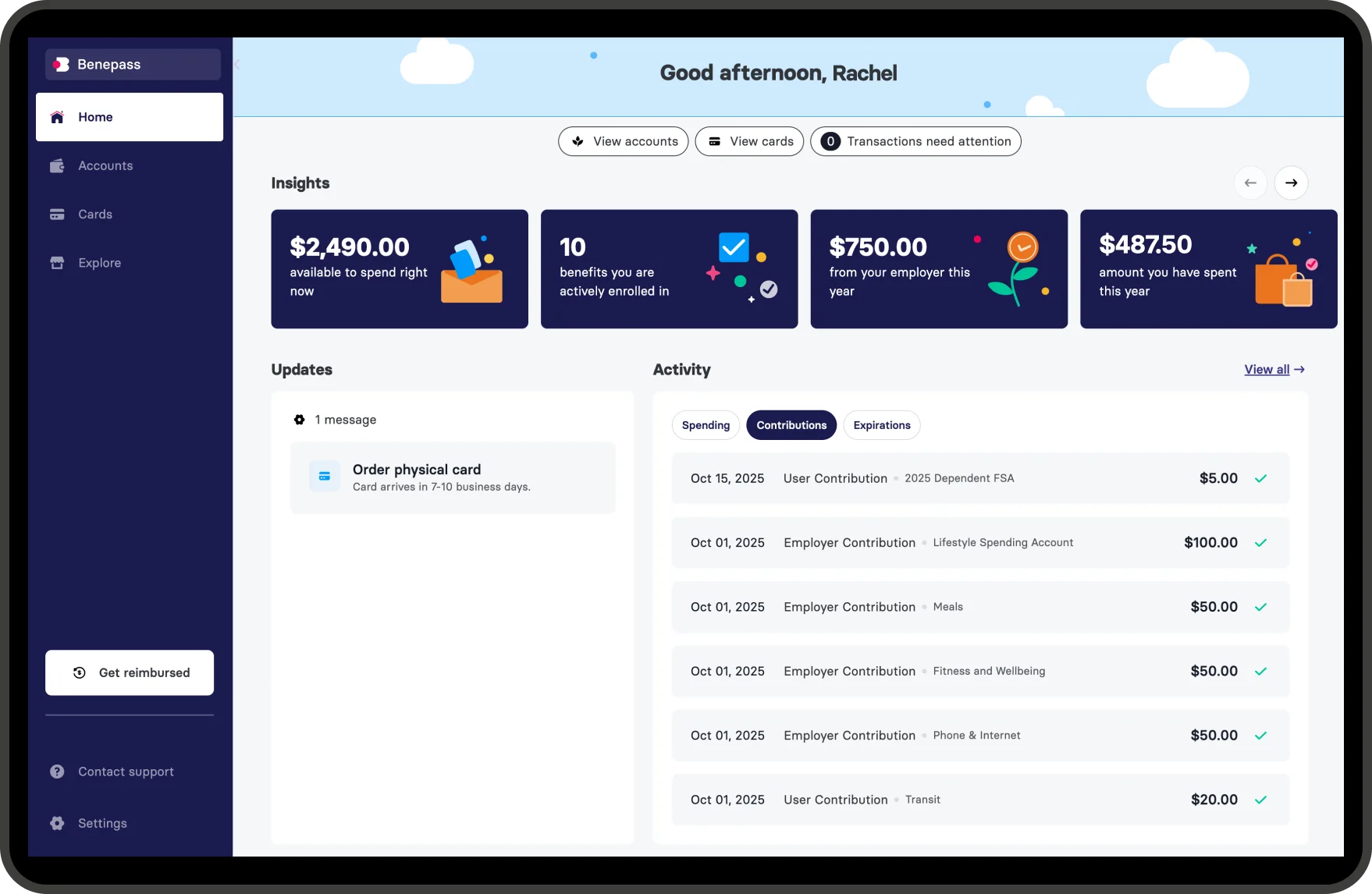

You also get clearer visibility into how benefits dollars are being used. Because you’re no longer piecing together reports across vendors, you can track spend in one place and use that data to make more informed decisions about future investments.

Predictable budget management

LSAs give you a level of cost control that’s difficult to achieve with traditional reimbursement-based benefits. Since you set a fixed amount per employee up front, you know your maximum exposure from day one, so you can avoid uncapped reimbursement risk and plan benefits spend with more confidence.

Median annual LSA contributions range from $500 for recognition programs to $1,200 for work-from-home, illustrating how program design shapes the investment employers make. Unused funds can roll over or return to your budget, depending on your policy. If you choose to go without rollovers, 15%–25% of funds may go unused, reducing net program cost.

However, when calculating ROI, the value of an LSA isn’t just in cost control. It’s in how that spend impacts employee engagement and retention.

- Replacing an employee can cost an average of $45,236

- Retaining even a small number of employees can offset the full cost of the program

To measure impact, track:

- Participation rates

- Retention among LSA participants vs. non-participants

- Which categories employees actually use

What are the main drawbacks of lifestyle spending accounts?

LSAs come with real limitations that HR leaders should evaluate honestly before implementation. Understanding these challenges helps you design a program that balances flexibility with control.

Tax implications and compliance complexity

Unlike pre-tax benefits such as HSAs or FSAs, most LSA contributions are considered taxable income to employees. When you fund an LSA, the IRS treats those dollars as imputed income. You'll need to:

- Report LSA funds on employee W-2 forms

- Withhold appropriate federal, state, and local taxes

- Ensure your payroll system can handle mid-year benefit adjustments

A $1,000 annual LSA allocation may translate to roughly $650–$750 in net purchasing power, depending on the employee's federal, state, and FICA tax rates. This gap between the stated benefit amount and net value can create confusion if not communicated clearly up front.

LSAs do require coordination between the finance and payroll teams to ensure accurate reporting, particularly when combined with other taxable benefits. To do this, you’ll need to factor in some additional payroll integration during implementation so everything runs smoothly post-launch.

Administrative oversight and fund management

Managing an LSA program also requires ongoing oversight to prevent misuse while maintaining the flexibility that makes these accounts valuable. Without proper controls, you risk:

- Employees purchasing items outside your intended categories

- Inconsistent approval processes across regions

- Limited visibility into utilization patterns

Manual reimbursement processes can require additional oversight, especially as usage grows. As employees submit receipts, your team spends time reviewing purchases against program rules and processes payments, which can add up at scale.

Setting clear guidelines from the start, defining eligible categories, and documenting approval workflows keeps administration consistent and manageable.

Limited program flexibility and employee choice

Designing an LSA benefits program requires walking a fine line between flexibility and control. Make your spending categories too restrictive, and you limit the personalization that makes LSAs attractive. Make them too broad, and you risk compliance issues and budget overruns.

Overly restrictive programs often see low utilization. If your LSA only covers gym memberships and fitness classes, you'll miss employees who would prefer to spend those dollars on mental health services, professional development, or family care.

Overly broad categories create different problems: employees may interpret eligible expenses differently, leading to increased administrative burden and difficulty demonstrating ROI.

The solution is thoughtful category design based on your actual workforce demographics. Survey employees before launch, then create four to six broad but clearly defined spending pillars with specific examples of eligible and ineligible expenses. Even well-designed programs need periodic review as workforce needs evolve.

How do lifestyle spending accounts compare to traditional benefits?

Traditional wellness stipends typically cover a narrow category, like gym memberships, exercise equipment, or fitness classes, with a fixed reimbursement amount. They're simple to administer but limited in scope. Professional development budgets work similarly: employees submit receipts for approved learning expenses, but the categories are usually rigid and managed separately from other benefits.

LSAs consolidate multiple programs into a single account. The trade-off is that LSAs are taxable, while some traditional benefits, like commuter benefits or FSAs, carry pre-tax advantages. LSAs also require more up-front design work to define categories and set spending rules.

LSAs tend to be most effective when your workforce is:

- Diverse in age, life stage, or work arrangement

- When you're managing multiple separate stipend programs that create administrative overhead

- When employees are asking for more flexibility in how they use their benefits dollars

If your workforce is relatively homogeneous and your current benefits see strong participation, a targeted stipend may deliver more value with less complexity than a full LSA program.

Should your organization implement a lifestyle spending account?

The decision to implement an LSA requires a clear-eyed evaluation of your organization's needs, workforce composition, and administrative capacity. Here are four key factors to work through before committing.

1. Evaluate business needs

Start by identifying the gaps in your current benefits offering:

- Are you seeing low engagement with existing perks?

- Are employees requesting more flexibility?

- Do you have a distributed workforce that can't access location-specific benefits equally?

These are the signals that an LSA might address real needs rather than create new overhead.

Connect those gaps to measurable business outcomes. If your goal is to reduce turnover, understand whether benefits flexibility actually moves the needle on retention in your industry.

2. Assess your workforce demographics

Your workforce composition directly shapes which benefits will drive the highest engagement. Map out who your employees are, where they work, and what life stages they're navigating.

If 40% of your workforce has young children, childcare and family care categories become strategic priorities. If you have a significant remote workforce, home-office equipment and coworking memberships may matter more than commuter benefits.

Run a demographic audit using your HRIS data to identify patterns rather than designing the program around leadership preferences. The most effective LSA programs reflect the real composition of your workforce, not assumptions about what most people want.

3. Analyze budget and administrative capacity

Run the numbers on both cost and operational requirements. Your number will depend on the categories you include and your competitive positioning. Factor in platform fees and budget for the administrative time required to track and report imputed income.

Assess your team's readiness honestly. Consider if you have the systems to:

- Automate eligibility tracking

- Integrate with payroll for tax reporting

- Provide self-service tools for employees

Manual processes don't scale well with LSAs. If your HR team is already at capacity, you'll need either a platform that automates these tasks or additional headcount. Compliance considerations, including IRS imputed income rules, payroll tax handling, and avoiding inadvertent ERISA or group health plan triggers if categories include medical expenses, should be factored into this assessment rather than treated as a separate step.

4. Gather employee input and feedback

Before rolling out any benefit, ask your employees what they actually want. Direct input helps you tailor the program to real preferences rather than assumptions and builds buy-in before launch.

A short survey can surface priorities you might not anticipate, with pointed questions like:

- Which spending categories would be most valuable to you?

- Would you prefer a single flexible account or multiple targeted stipends?

If you're uncertain about full-scale adoption, consider piloting an LSA with one department or location for three to six months. Measure utilization rates, satisfaction scores, and feedback before committing to a company-wide rollout.

Getting started with lifestyle spending account implementation

If your evaluation points toward an LSA, take the time to build a program that works for your organization and employees.

Start by defining spending categories that reflect your workforce and company priorities, then set clear eligibility guidelines with specific examples. From there, outline your budget and policy structure:

- Set your allocation based on benchmarking data and overall benefits spend

- Decide whether unused funds roll over or return to the business

- Communicate tax treatment clearly so employees understand the net value of the benefit

But keep in mind that the right approach depends on your workforce, your goals, and your operational capacity.

Platforms like Benepass help employers smoothly implement LSAs with built-in controls, real-time visibility, and a simpler experience for both employees and admins—no matter what approach you choose.

Explore the Benepass lifestyle spending account to see how flexible benefits can work for your organization.

Frequently Asked Questions

Rebecca Noori

Rebecca Noori is a freelance HR Tech and SaaS writer who is obsessed with our world of work. She writes about everything from employee benefits and performance management to upskilling and productivity tips. When she's not writing, you'll find her grappling with phonics homework and football kits, looking after her three kids.