In this post

Lorem ipsum dolor sit amet

Lorem ipsum dolor sit amet

The HSA market is rapidly expanding, and the provider you choose today will have a lasting impact on your employee benefits strategy. Benepass’s 2026 Benefits Benchmarking Report found that 61% of employers currently offer an HSA, underscoring how common these accounts have become in modern benefits design. For HR leaders, this rapid growth makes vendor selection a critical strategic decision.

To help you navigate this landscape, this guide compares five leading HSA providers, outlines key features to evaluate, and breaks down common pricing models so you can make a confident final decision.

What is an HSA provider?

An HSA provider is the institution or platform that administers your company's Health Savings Account program for enrolled employees. These accounts help employees set aside tax-free money for qualified medical expenses, including many everyday healthcare expenses not fully covered by a health insurance plan.

Your HSA provider shapes how efficiently your team manages benefits, how engaged employees are with their accounts, and how well you stay compliant with IRS rules:

- Administrative efficiency: Modern HSA providers automate enrollment, contribution processing, and eligibility tracking through direct integrations with your payroll and HRIS systems. This eliminates manual file uploads and reduces errors, which frees your team from repetitive tasks.

- Employee engagement: The best HSA providers deliver digital experiences that make it easy for employees to understand and use their accounts for eligible expenses. Higher engagement translates to better financial wellness outcomes and stronger ROI.

- Compliance and risk management: HSA administration involves strict IRS contribution limits, eligibility rules, and reporting requirements. A strong provider builds compliance guardrails into the platform and automatically flags issues before they become audit risks.

For organizations managing multiple benefit types, some modern HSA providers like Benepass offer unified platforms that consolidate HSAs, FSAs, LSAs, and commuter benefits into a single system. This reduces vendor complexity and consolidates reporting, giving employees one place to manage all their tax-advantaged accounts.

Key features to evaluate when selecting HSA providers

Choosing an HSA provider is about finding a partner that reduces manual work for HR and makes it easier for employees to use and understand their benefits. As you compare vendors, focus on the features that will have the biggest impact on day-to-day administration and long-term scalability. This includes:

- Integration capabilities: Ask whether the provider offers real-time API connections or relies on batch file uploads. Request a list of compatible payroll and HRIS systems, and confirm how mid-year eligibility changes are handled.

- Employer reporting and analytics: Ask to see sample dashboards. Verify whether you can export data in formats your finance team uses and whether participation trends are visible at the account level.

- Transparency and fee structure: Request a complete fee schedule, including charges for investment options, card replacements, and customer support calls. Many providers advertise low base rates but add fees that compound quickly at scale.

- Employee experience: Ask about mobile app ratings, average reimbursement time, and whether the platform supports multiple languages. Providers with modern interfaces typically see higher participation rates.

- Scalability: Confirm whether pricing changes as you grow and whether the provider can support multi-state compliance or additional account types without requiring a platform migration.

5 best HSA providers for businesses in 2026

Here's how leading platforms compare and what HR leaders should know before making a selection.

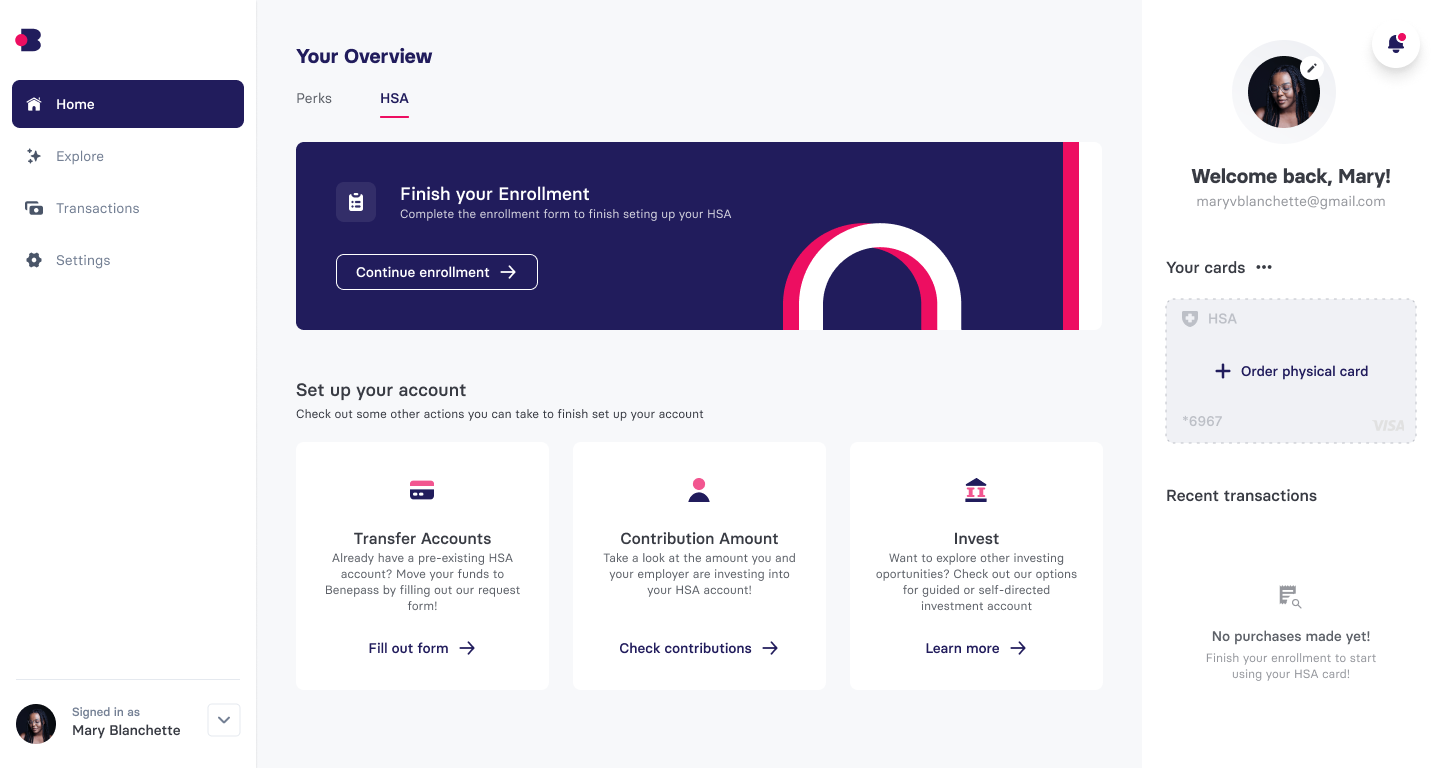

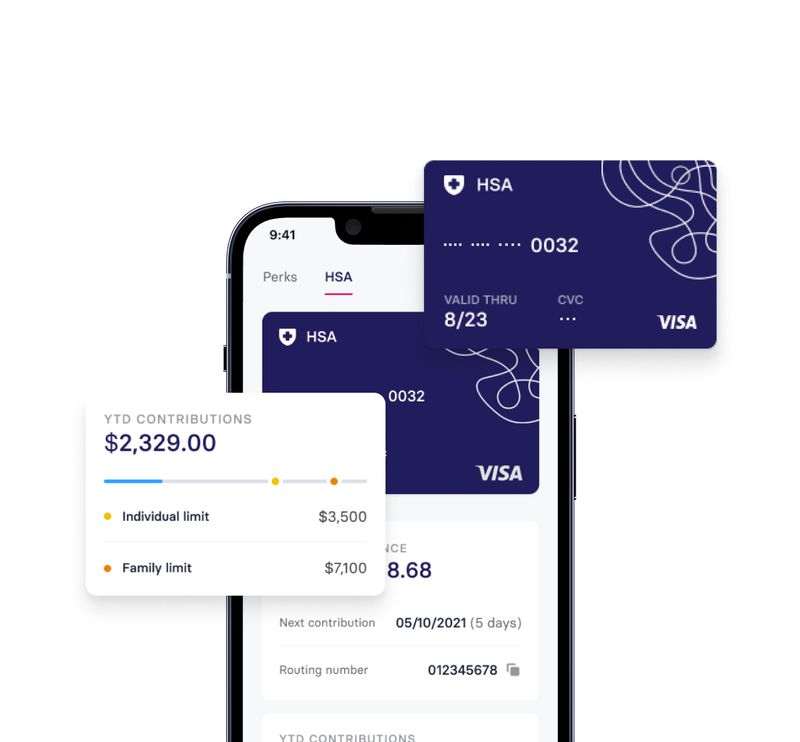

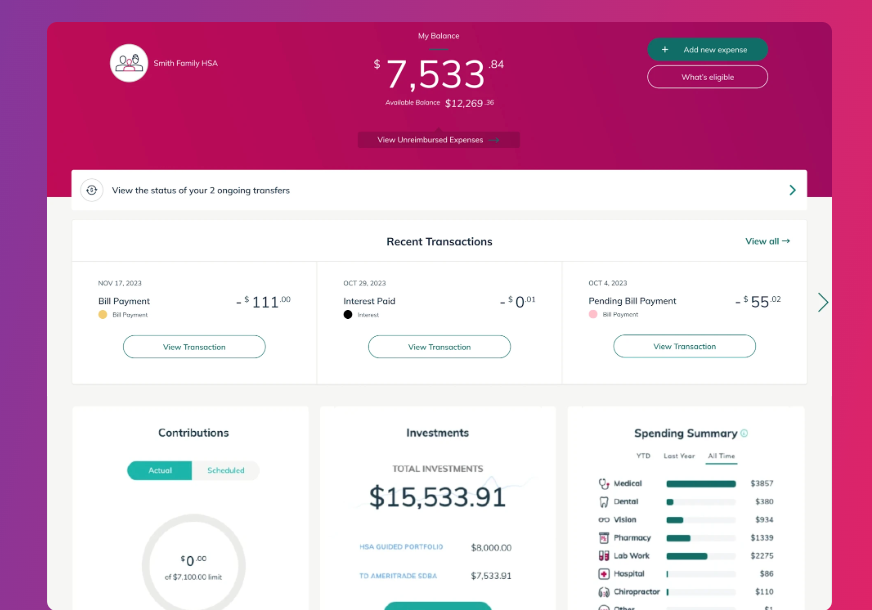

1. Benepass

Best for: Mid-sized and enterprise employers looking to modernize benefits administration and drive employee engagement across multiple account types.

Benepass unifies HSAs, FSAs, LSAs, and commuter benefits on a single platform. This consolidation reduces vendor complexity for HR teams, gives employees a single wallet for all their spending, and automates enrollment and contributions via a direct payroll connection.

Why it stands out

Over 25% of Benepass HSA holders use their accounts for HSA investment, compared to industry averages of 7–10%. That gap comes from a low barrier to investing, transparent pricing, and the ability to manage HSA funds directly in an integrated investment account experience. The platform holds a 97% customer satisfaction rate.

- Automated HRIS and payroll integration for enrollment and contributions

- Unified benefits experience across HSAs, FSAs, LSAs, and commuter benefits

- Low investment barrier with a $125 minimum and no hidden fees

- SOC 2 certification and bank-level encryption

- Custom pricing based on organization size and benefit mix

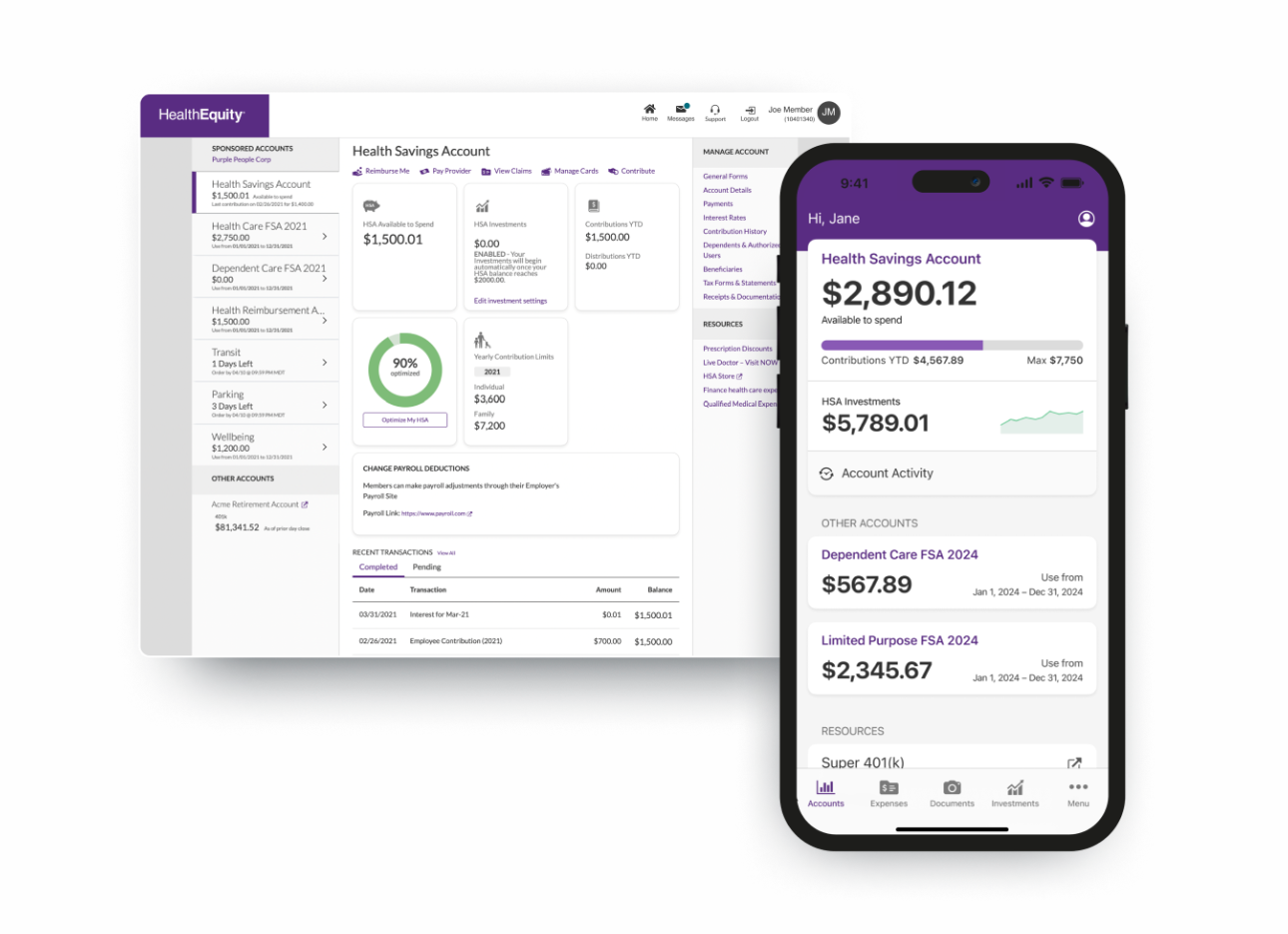

2. HealthEquity

Best for: Compliance-sensitive organizations in regulated industries that need a proven partner with strong security and regulatory support.

With 9.9 million HSAs and 17.1 million total accounts as of April 2025, HealthEquity brings the scale and infrastructure that large employers need. The platform covers HSAs, HRAs, FSAs, COBRA, and commuter benefits, making it a viable option for organizations that want a single administrator with deep compliance expertise.

Why it stands out

HealthEquity integrates with existing health plans, retirement providers, and payroll systems, simplifying data flows and reporting. The platform includes 24/7 member services and the Engage360 education suite for benefits professionals.

- Comprehensive administration across HSAs, FSAs, HRAs, COBRA, and commuter accounts

- Integrated data workflows across payroll, health plans, and retirement providers

- 24/7 live support and Engage360 education resources

- Security architecture with encryption, biometric login, and 2FA

- Pricing requires a direct quote, and often includes monthly per-account fees plus potential investment management charges

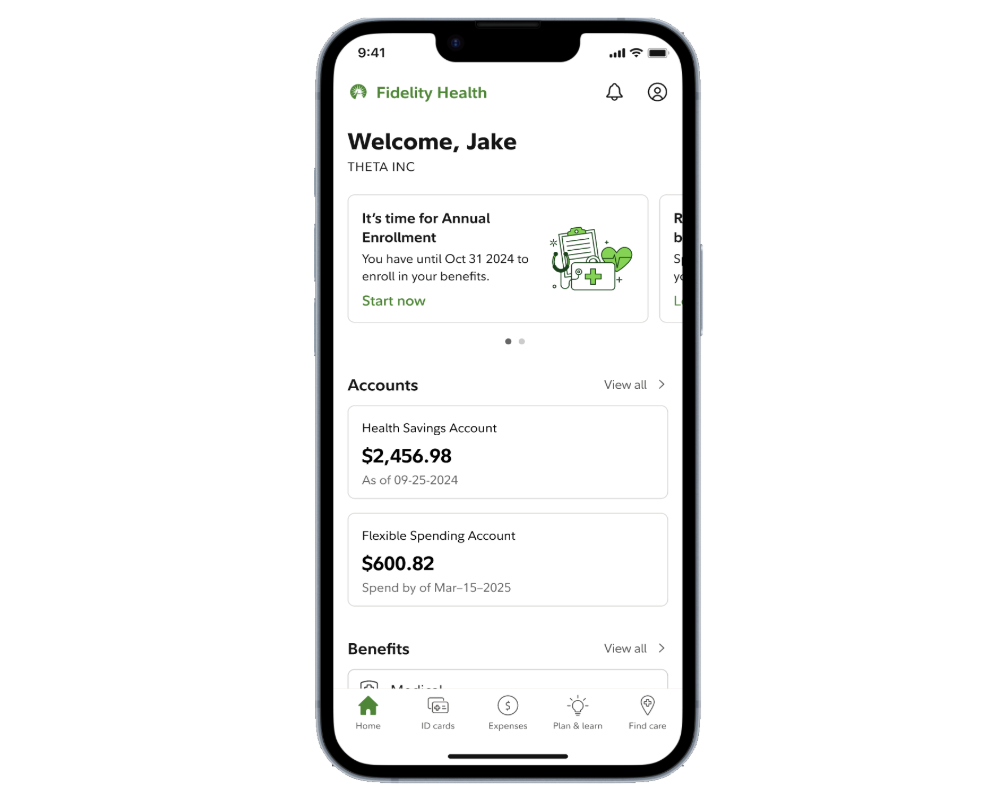

3. Fidelity HSA

Best for: Employers that prioritize brand trust and financial wellness alignment, particularly those already using Fidelity for retirement benefits.

With more than 4.4 million HSA account holders and high marks from Morningstar's 2025 HSA provider assessments, Fidelity combines decades of investment expertise with a proven employee-facing experience. The no-fee structure makes it particularly attractive for cost-conscious employers.

Why it stands out

The Fidelity HSA integrates with the Fidelity Plan Sponsor WebStation (PSW) employer dashboard and the NetBenefits employee platform, so HR teams can manage HSAs and retirement plans side by side. There are no account fees, no minimums to open, and a wide range of investment options from mutual funds to self-directed brokerage.

- Deep integration with Fidelity's retirement savings and investment platforms

- Zero account fees for both employers and employees, no minimum investment

- Mutual fund and self-directed brokerage investment options

- Data-driven employee education tools to drive utilization

4. Lively

Best for: Mid-sized employers and tech-forward teams that prioritize flexible integrations and transparent pricing.

Lively's technology is built in-house, which means the platform offers real-time API connections, SFTP data feeds, and Single Sign-On without relying on legacy infrastructure. For HR teams that want to automate enrollment and contribution workflows without overhauling their existing tech stack, that flexibility is a key benefit.

Why it stands out

Each employer is paired with a dedicated customer success team for onboarding and ongoing support. Employees reach member support via phone, email, or chat year-round. Transparent pricing at $2.95 per employee per month (subject to a $200 monthly minimum) makes budgeting predictable.

- Real-time API, SFTP, and SSO integration options

- Dedicated Customer Success team for onboarding and ongoing admin support

- Transparent pricing: $2.95 PEPM with no add-on fees

- Intuitive admin dashboard for contribution management and reporting

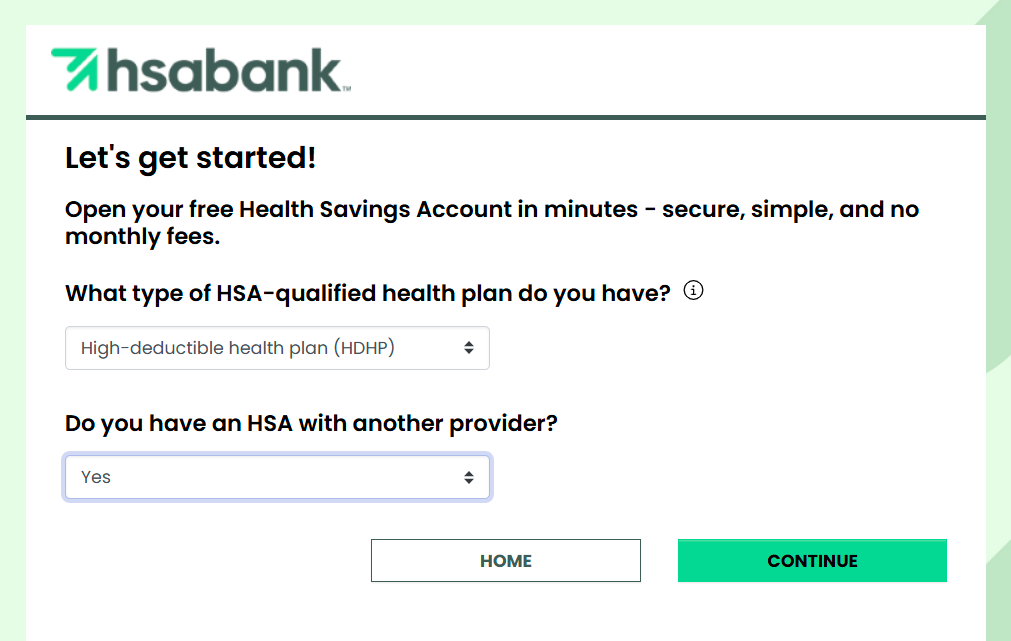

5. HSA Bank

Best for: Employers seeking a straightforward HSA partner backed by a stable financial institution.

As a division of Webster Bank, N.A., HSA Bank combines more than two decades of experience with the financial stability of a nationally chartered bank. Because HSA Bank acts as both the custodian and the administrator, you avoid the confusion that comes with custodial changes, a common pain point when switching providers.

Why it stands out

HSA Bank supports HSAs, FSAs, HRAs, LSAs, commuter benefits, and tuition reimbursement programs. The Health Benefits Debit Card provides 85-95% auto-substantiation rates, reducing paperwork and increasing employee participation.

- Backed by Webster Bank's financial infrastructure for long-term stability

- Flexible enrollment options and four contribution workflows

- One-stop custodian and administrator for added continuity

- HSA Invest program with mutual funds and self-directed brokerage once balance thresholds are met

- Pricing follows an annual asset-based fee structure starting at 0.1%

Cost structure and pricing models of HSA providers

For employers, choosing a provider with transparent pricing and low fees can make a meaningful difference in how employees prepare for future healthcare costs and out-of-pocket healthcare expenses. HSA provider pricing varies significantly, but the three most common models are:

- Per-employee-per-month (PEPM): A flat fee charged for each enrolled employee, regardless of account balance. This model is predictable and easy to budget, especially for organizations with lower average balances.

- Asset-based fees: A percentage of assets under management, typically ranging from 0.1% to 0.5% annually. This model can be cost-effective for employers with high average balances, but it becomes expensive as accounts grow.

- Custom or bundled pricing: Providers like Benepass and HealthEquity offer custom quotes based on organization size, benefit mix, and integration requirements. These arrangements often bundle multiple account types, which can reduce per-unit costs for employers consolidating vendors.

Beyond the base fee, ask every vendor about transaction fees, investment management charges, debit card replacement costs, and whether customer support calls carry a per-incident fee.

How to switch or set up HSA providers

Switching HSA providers is manageable with the right planning. Here's how a realistic timeline looks and what to address at each stage.

Pre-implementation planning (weeks 1–2)

Start with a full audit of your current program before making any changes.

- Document your setup: This includes payroll integrations, contribution schedules, and mid-year enrollment rules.

- Confirm system compatibility: Ensure your new provider works with your HRIS and payroll systems.

- Identify impacted employees: Flag any accounts with invested funds that will need to be liquidated or transferred.

Data migration (weeks 2–4)

Most providers will require a defined set of employee and plan data.

- Prepare required files: Compile employee demographics, contribution history, and eligibility data.

- Clarify responsibilities: Confirm whether the provider handles migration or if your team uploads files.

- Plan for existing balances: Understand how HSA funds will be transferred and whether a rollover is required.

- Ask about blackout periods: Confirm whether there will be any temporary withdrawal restrictions during the transition.

Employee communication (weeks 3–5)

Clear, timed communication reduces confusion and support volume.

- Send a 30-day notice: Explain what’s changing, when it’s happening, and what employees need to do.

- Set expectations: Include details on account access, debit card delivery, and any temporary spending limits.

- Reinforce before launch: Send a reminder one week before go-live to reduce support tickets.

Making your final HSA provider decision

Once you've narrowed your list to two or three vendors, the decision usually comes down to three factors: how well the platform fits your existing tech stack, whether the employee experience will drive actual utilization, and whether the total cost of ownership aligns with your budget.

Use this framework to compare your finalists:

- Integration fit: Does the provider connect directly to your payroll system via API, or will your team manage file uploads?

- Utilization potential: Request participation data from each vendor. Providers with mobile-first designs and low investment minimums consistently show higher engagement.

- Total cost of ownership: Model your costs over 24 months using your actual headcount and expected account growth. Include all fees, not just the base rate.

- Vendor consolidation opportunity: If you're managing separate vendors for HSAs, FSAs, and lifestyle benefits, a unified platform can simplify operations and enhance the employee experience.

The right HSA provider should reduce the day-to-day burden on your team. It should also give employees a reliable way to use their funds, and give you clear visibility into every dollar. That’s where most legacy providers fall short.

With Benepass, you can consolidate pre-tax accounts into a single unified system. If you’re managing separate vendors for HSAs, flexible spending accounts, and lifestyle benefits, this can simplify operations and improve the employee experience. The result is a benefits program you can confidently stand behind.

Schedule a demo to walk through the Benepass platform and explore what implementation looks like for your team.

Frequently Asked Questions

Rebecca Noori

Rebecca Noori is a freelance HR Tech and SaaS writer who is obsessed with our world of work. She writes about everything from employee benefits and performance management to upskilling and productivity tips. When she's not writing, you'll find her grappling with phonics homework and football kits, looking after her three kids.

.jpg)