In this post

Lorem ipsum dolor sit amet

Lorem ipsum dolor sit amet

WEX is best known by many HR leaders for its fleet card and fuel payment business, but it also administers pre-tax accounts (HSAs, FSAs, HRAs, and COBRA) for employers across the United States. Teams evaluating alternatives are usually weighing whether a pre-tax account administrator still suits their business when newer platforms can consolidate those accounts alongside commuter benefits and lifestyle stipends, all on a single card and system.

Switching administrators isn't a small decision. It touches payroll operations, employee experience, compliance posture, and your ability to measure utilization across every program you offer.

This guide walks through how to evaluate WEX alternatives against the criteria that matter, compare leading platforms side by side, and build a viable business case for finance and executive stakeholders.

What is WEX, and why are HR teams looking for alternatives?

WEX benefits administration covers a range of pre-tax accounts designed to help employers offer tax-advantaged savings programs. It operates primarily as a pre-tax account administrator rather than a consolidated benefits platform, which is one reason why teams may look elsewhere when goals change.

What do WEX benefits cover?

WEX administers:

- Health Savings Accounts (HSAs)

- Flexible Spending Accounts (FSAs), including Limited Purpose FSAs and Dependent Care FSAs

- Health Reimbursement Arrangements (HRAs)

- Lifestyle Spending Accounts (LSAs)

- Commuter benefits for transit and parking under IRS Section 132(f), ICHRA (Individual Coverage HRA), VEBA, and tuition reimbursement

- COBRA continuation coverage

WEX has added LSAs to its platform, but the experience is built on a traditional pre-tax administration foundation rather than a card-first, configurable model. Employers running modern LSA programs (with custom categories, real-time policy enforcement, and global card acceptance) often find that bolting LSAs onto a legacy pre-tax platform doesn't deliver the same employee experience as a purpose-built platform.

What are the most common reasons HR teams switch away from WEX?

- Limited program flexibility: WEX offers commuter benefits and LSAs alongside its core pre-tax accounts, but the platform is built on a legacy pre-tax administration foundation. Employers running modern LSA or stipend programs often find the employee experience doesn't keep up with purpose-built platforms.

- Integration gaps: WEX offers integrations with major payroll providers, but depth and reliability vary. When integrations require manual file uploads or weekly batch processing, your team absorbs the administrative cost and the risk of compliance errors.

- Pricing opacity: WEX's fee structure can include per-participant-per-month charges, transaction fees, and additional costs for COBRA or customer support. If you can't model total cost of ownership up front, it's harder to defend your budget internally.

- Service gaps: When your benefits administrator doesn't offer proactive compliance support or clear audit trails, your team fills the gap by fielding employee questions about declined transactions, manually tracking substantiation requests, and troubleshooting without clear escalation paths.

How to evaluate WEX benefits alternatives: A framework for HR teams

Platforms in this space vary widely in account coverage, compliance depth, integration quality, and pricing transparency. Those differences quickly become clear in administrative hours, employee participation, and total cost of ownership.

These four criteria give you a clear, repeatable way to compare WEX alternatives side by side.

Benefits account administration (HSA, FSA, HRA, commuter, and COBRA)

The first question to answer is which account types each platform supports. Most WEX alternatives handle HSAs and FSAs, but not all extend to HRAs, limited-purpose FSAs, dependent care FSAs, commuter benefits, or COBRA. Confirm that any platform you're evaluating supports your current account mix and can add new account types as your benefits strategy evolves.

Compliance posture (HIPAA, ERISA, IRS substantiation, and audit trails)

Your benefits platform is a compliance partner, not just a payment processor. Any platform administering health-related accounts must be HIPAA-compliant and willing to sign a Business Associate Agreement. Beyond that, confirm the vendor automates IRS substantiation using merchant category codes and receipt capture, maintains ERISA-compliant plan documentation, and generates exportable audit logs that hold up under DOL or IRS review.

HRIS and payroll integrations (ADP, Workday, UKG, and Paychex)

Without native integrations, you're looking at manual file uploads, reconciliation errors, and hours of administrative work each pay period. The best platforms offer pre-built connectors to popular platforms and services, like ADP Workforce Now, Workday, UKG, and Paychex, with bi-directional data sync that automates eligibility updates, contribution deductions, and enrollment changes.

Ask each vendor how often data syncs, what happens when an employee terminates mid-period, and whether your IT team needs to build or maintain any customizable connections.

Pricing transparency and fee structure

Benefits administration pricing is notoriously opaque. Many vendors quote a per-employee-per-month (PEPM) rate but layer on transaction fees, account maintenance fees, COBRA administration fees, and implementation charges. Ask vendors for a total cost estimate based on your actual employee count and benefit mix, not just a base rate.

Platforms like Benepass use a clear PEPM model that covers pre-tax accounts, lifestyle benefits, and commuter benefits on one card with no hidden transaction fees, which makes forecasting costs and defending your budget internally much more straightforward.

WEX alternatives compared: Top platforms for HR teams in 2026

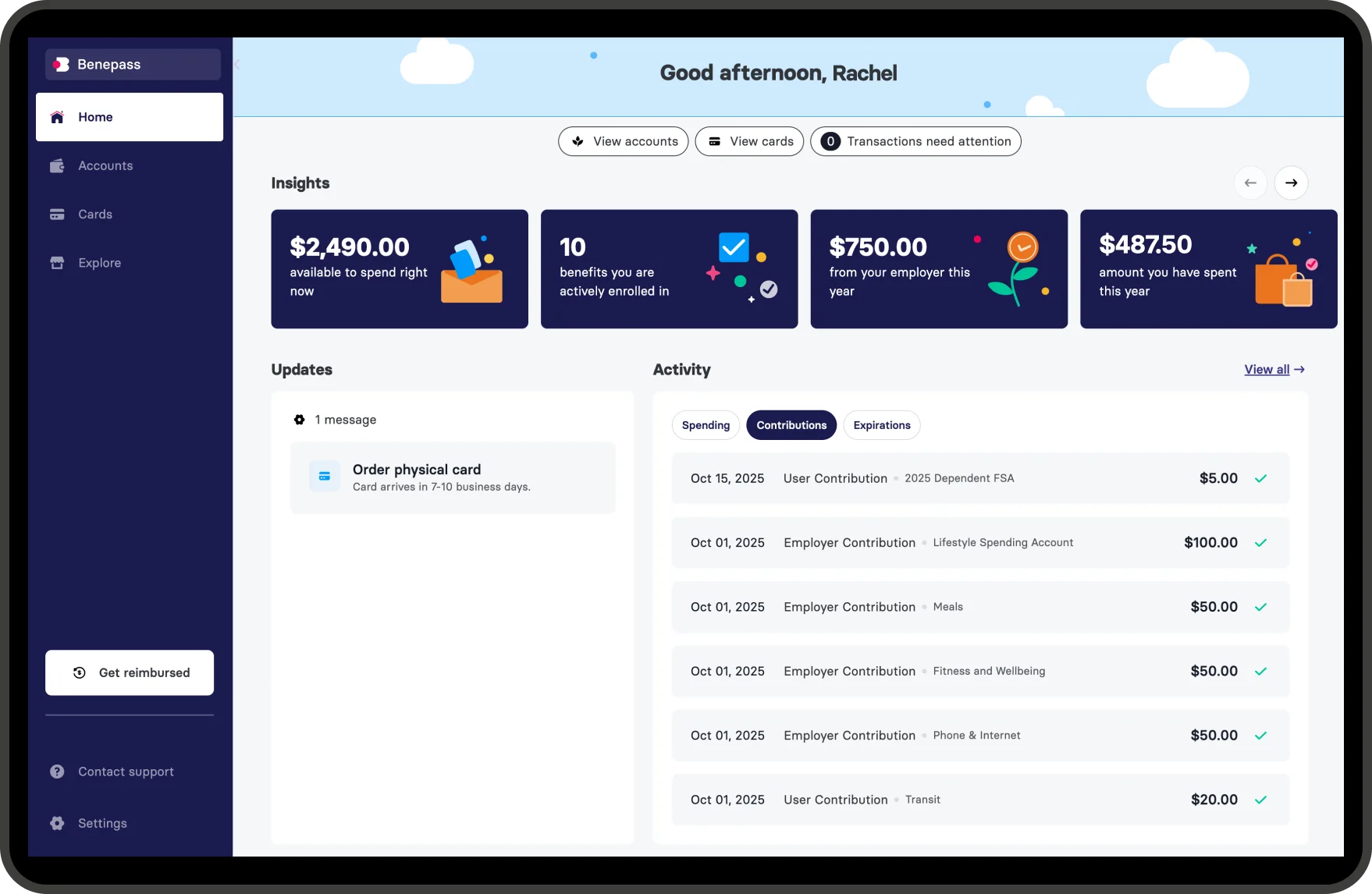

Benepass

Benepass consolidates pre-tax accounts and flexible benefits into a single platform. Instead of managing separate vendors for HSA, FSA, HRA, commuter benefits, and lifestyle stipends, you get one platform, one card, and one employee experience.

According to Benepass's 2026 Benefits Benchmarking Report, 37% of Benepass clients now run both pre-tax and LSA benefits on a single platform, and those employers see higher FSA utilization than fragmented programs (85% vs. 79%).

- Accounts covered: HSA, FSA (healthcare, limited-purpose, dependent care), HRA, commuter benefits, COBRA, and lifestyle stipends

- Compliance: HIPAA and ERISA compliant, with automated IRS substantiation and full audit trails for every transaction

- Integrations: Native connectors to ADP, Workday, UKG, and Paychex with two-way data syncing

- Employee experience: Single card for all accounts, mobile app with real-time balances and eligible expense tracking; 80%+ benefit utilization across 500,000+ users in 90+ countries

- Pricing: Transparent PEPM with no hidden fees, account minimums, or transaction charges

Benepass maintains a 98% client retention rate, which is a useful signal when you're trying to avoid another migration in two years. If you're managing multiple pre-tax accounts or running lifestyle stipends alongside traditional benefits, Benepass is worth evaluating as a consolidation play.

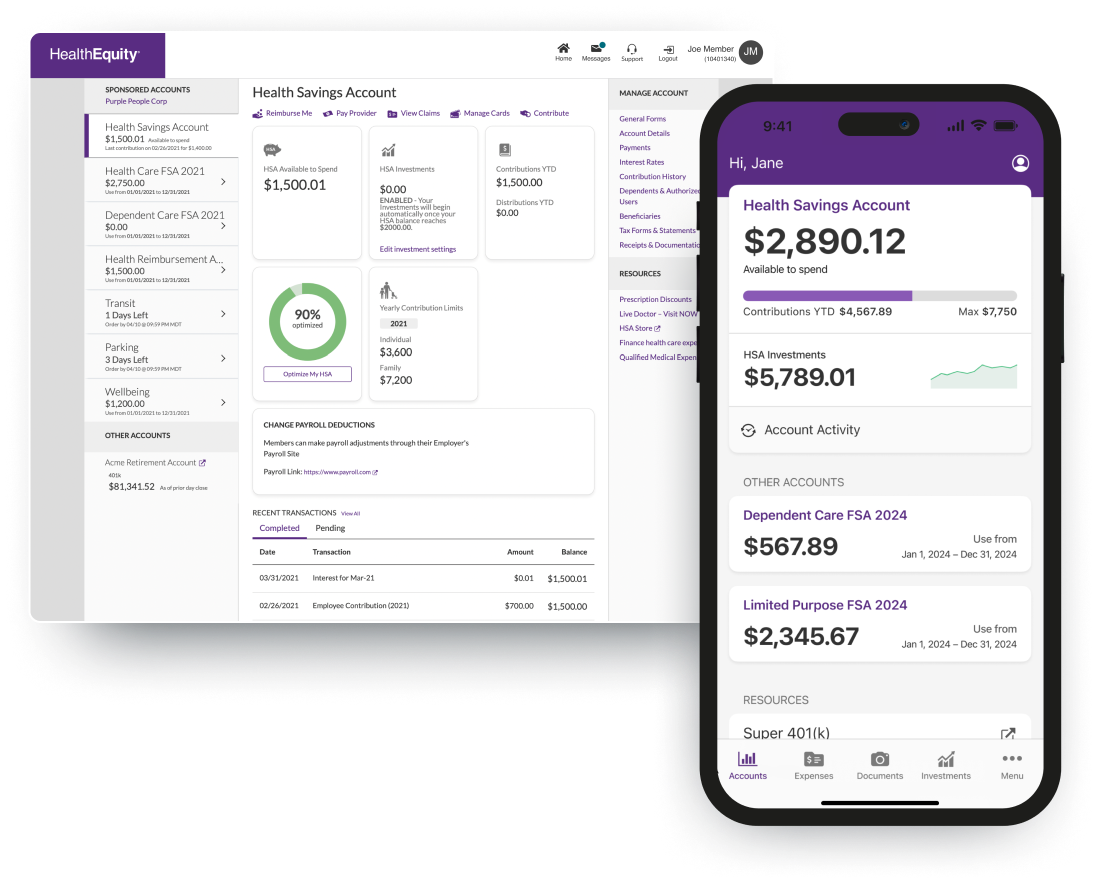

HealthEquity

HealthEquity is the largest HSA custodian in the US, but that focus also limits variety.

- Accounts covered: HSA, FSA (healthcare, limited-purpose, dependent care), HRA, commuter, and COBRA

- Compliance: HIPAA and ERISA compliant with carrier integrations that automate FSA and HRA substantiation

- Integrations: Connects to ADP, Workday, and UKG; some HR teams report setup can take longer than expected

- Limitations: Fee structure can be difficult to predict across multiple account types, and HealthEquity's LSA offering is newer and less configurable than purpose-built lifestyle platforms

HealthEquity is a strong fit if HSA investment options are a priority and you're comfortable managing commuter and lifestyle programs through separate vendors.

Inspira Financial

Inspira Financial (the rebrand of Millennium Trust Company after its acquisitions of PayFlex, Benefit Resource, and others) positions itself as a full-service provider for employers that want pre-tax, benefits, and retirement administration under one vendor relationship.

- Accounts covered: HSA, FSA (healthcare, limited-purpose, or dependent care), HRA, commuter benefits, COBRA, and retirement services

- Compliance: HIPAA, ERISA, and IRS compliant with automated substantiation workflows

- Integrations: Connects to ADP, Workday, UKG, and Paychex; integration depth varies by payroll provider and may require custom file formats

- Limitations: Generating custom compliance reports may require support team involvement; total cost of ownership can increase as you add account types

Inspira Financial works well for employers that need traditional benefits administration alongside retirement plan capabilities. If a modern employee experience or consolidated lifestyle benefits are priorities, a purpose-built platform may serve you better.

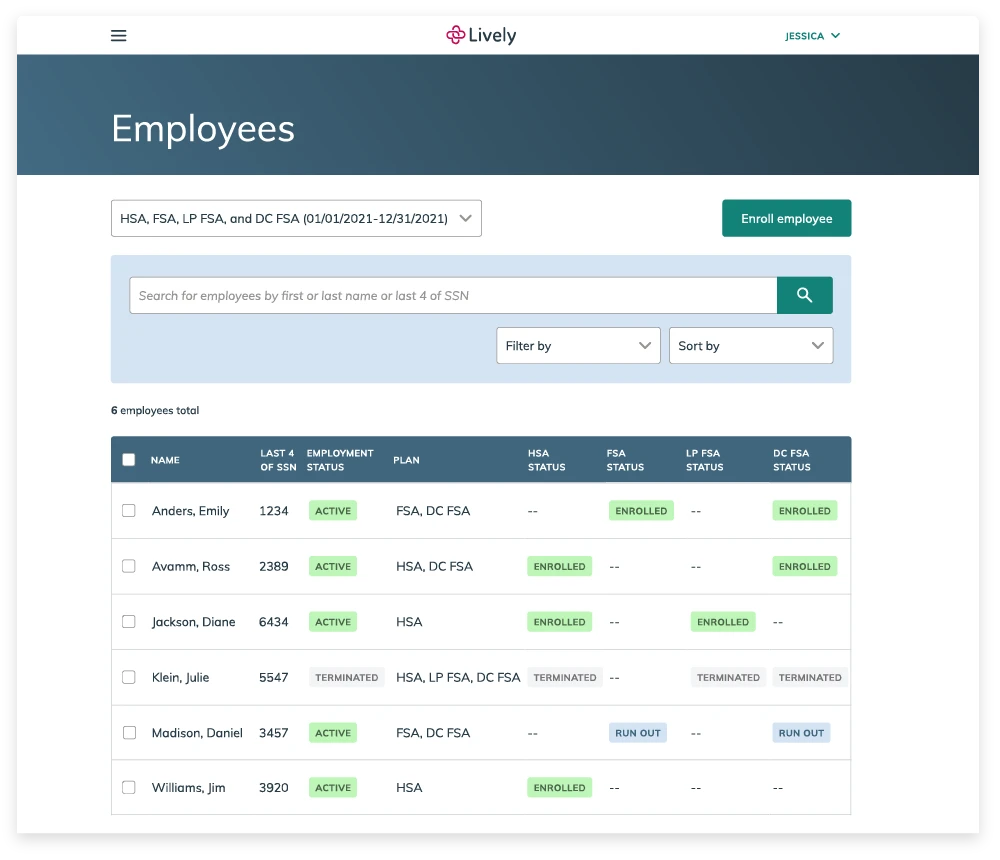

Lively

Lively is a digital-first HSA administrator built for small to mid-sized employers who want a low-cost, straightforward health savings account solution with no monthly fees for employees.

- Accounts covered: HSA, FSA (healthcare, limited-purpose, dependent care), HRA, LSA, Medical Travel Accounts, commuter benefits, and COBRA

- Compliance: HIPAA compliant with IRS substantiation and audit trails

- Integrations: Connects to ADP, Gusto, and Paychex; limited support for Workday, UKG, or less common payroll providers

- Limitations: Automated payroll and HRIS file feeds require a minimum of 250 benefit-eligible lives, which can be a constraint for smaller employers or those scaling up; integration depth varies by payroll provider

Lively is a viable option if your primary need is a simple, low-cost HSA administrator and you're comfortable managing other benefit accounts through separate vendors. For employers needing global card acceptance, real-time policy enforcement on lifestyle stipends, or fully integrated post-tax and pre-tax programs on one card, a platform with deeper card-first infrastructure may fit better.

Rippling

Rippling offers benefits administration as part of a broader workforce management platform that combines payroll, HR, IT, and benefits into a single system.

- Accounts covered: HSA, FSA (healthcare and dependent care), and commuter benefits, integrated with medical, dental, vision, and 401(k) enrollment, plus automated ACA and COBRA compliance

- Compliance: HIPAA compliant with IRS substantiation and audit trails built in

- Integrations: Native payroll and HRIS built into the same platform, eliminating third-party connections for Rippling payroll users

- Limitations: Benefits administration is strongest when you use Rippling for payroll; if you're committed to ADP or Paychex, you lose much of the structural advantage, but bundled pricing makes it harder to evaluate benefits cost in isolation

Rippling fits mid-market employers who want to consolidate multiple HR systems and are willing to adopt Rippling's payroll and HRIS as the foundation. For organizations that need only pre-tax account administration or want to layer flexible benefits onto existing payroll systems, a dedicated benefits platform offers more flexibility.

Which WEX benefits alternative fits your organization?

The right platform depends on four factors: company size, workforce distribution, benefit program complexity, and whether you need a pre-tax-only solution or a broader flexible benefits platform.

Mid-market employers (500–2,500 employees) with a US-based workforce typically need a platform that handles HSA, FSA, HRA, and commuter accounts with strong payroll integration and straightforward pricing. Lively or HealthEquity work well if your focus is strictly pre-tax accounts. If you're also running stipend programs or lifestyle benefits, a consolidated platform like Benepass puts pre-tax and flexible benefits on one card and one admin system.

Enterprise employers (2,500+ employees) with multi-state or international teams should prioritize deep HRIS connectivity, robust compliance infrastructure, and support for global benefits. Benepass supports 400,000+ users across 90+ countries and consolidates pre-tax accounts, commuter benefits, and lifestyle programs into a single platform, reducing vendor sprawl and administrative overhead at scale.

Organizations running complex programs with multiple account types and wellness initiatives should look for platforms that consolidate vendors for simpler management. Frame your decision around measurable outcomes: budget utilization rates, employee participation rates, and administrative hours saved. These metrics matter more than feature lists when you're building an internal business case or defending a vendor switch to finance stakeholders.

How to build an internal business case for switching benefits administrators

Switching benefits administrators is a procurement decision and a people decision. Your business case needs to speak to cost, risk, and employee experience in equal measure.

Start by quantifying your current state. Document what you're paying WEX today, including not just the PEPM fee, but also transaction fees, COBRA administration charges, and any one-off costs for support or custom reporting. If you're running multiple vendors for HSA, FSA, commuter, and lifestyle benefits, add those contracts together. That total is your baseline.

Next, document the service gaps that are costing you time or participation. Track how many hours your benefits team spends each month on tasks like:

- Reconciling payroll files

- Answering employee questions about declined transactions

- Chasing down receipts for substantiation

If employees are underutilizing their accounts because the experience is clunky, calculate the dollars left on the table, like unused FSA funds, low HSA contribution rates, or commuter benefits that go unclaimed.

Then, project the ROI from a switch. Compare your current total cost to the pricing model of your top WEX alternatives. Factor in time savings from better integrations, higher participation from a more accessible employee experience, and reduced vendor management overhead from consolidation.

Finance and executive stakeholders care about cost per employee, budget utilization rates, and administrative efficiency. Show them the current state, the projected state, and the delta. If a new platform can increase FSA participation by 15% or save your team 10 hours per pay period, put those numbers in the deck.

If you’re looking to switch, consider Benepass for easy consolidation and management alongside flexible benefits. Benepass can map your specific program needs and build a smarter benefits setup, providing better ROI and a greater employee experience.

Frequently asked questions about WEX benefits alternatives

What is the difference between WEX Fleet Cards and WEX benefits?

WEX Fleet Cards and WEX benefits are separate product lines within the same company. WEX Fleet Cards manage fuel purchases and vehicle expenses for commercial fleets, while WEX benefits administers pre-tax benefit accounts like HSAs, FSAs, HRAs, and COBRA for employers. If you're evaluating WEX alternatives for benefits administration, you're looking at the health and benefits division specifically, not the fleet fuel card business.

How long does it take to migrate from WEX benefits to a new platform?

Most benefits administration migrations take 60 to 90 days from contract signature to go-live, though timelines vary based on your plan year timing, the number of account types you're moving, and how complex your payroll integrations are. You'll need to coordinate data transfers for existing HSA balances, set up new payroll deduction mappings, communicate the change to employees, and distribute new benefit cards.

Plan to start the migration process at least one full quarter before your target launch date to avoid rushing through compliance reviews or employee communications.

Does switching benefits administrators affect employee HSA balances or COBRA coverage?

Switching benefits administrators does not affect employee HSA balances or COBRA coverage rights. HSA funds belong to the employee and are fully portable, so balances transfer directly from your old administrator to the new one through a trustee-to-trustee transfer process that typically takes two to three weeks.

COBRA coverage continuation is a legal obligation that stays with the employer regardless of which vendor administers it, so employees mid-COBRA simply receive new payment instructions and benefit cards from the new platform. The key is to coordinate the transition carefully so there's no gap in claims processing or employee access to funds during the switchover period.

Frequently Asked Questions