In this post

Lorem ipsum dolor sit amet

Lorem ipsum dolor sit amet

Benefits programs are expanding, but employee expectations are moving faster. What worked as a one-size-fits-all approach a few years ago no longer holds up across a distributed, multi-generational workforce.

The result is familiar: low utilization, inconsistent engagement, and benefits that look good on paper but don’t get used in practice.

That’s why more HR teams are shifting toward flexible, employee-directed benefits that can adapt to different needs without adding more vendors or administrative overhead. This guide breaks down how LSAs work, where they fall short, and how to design a program that employees will actually use.

What are lifestyle spending accounts?

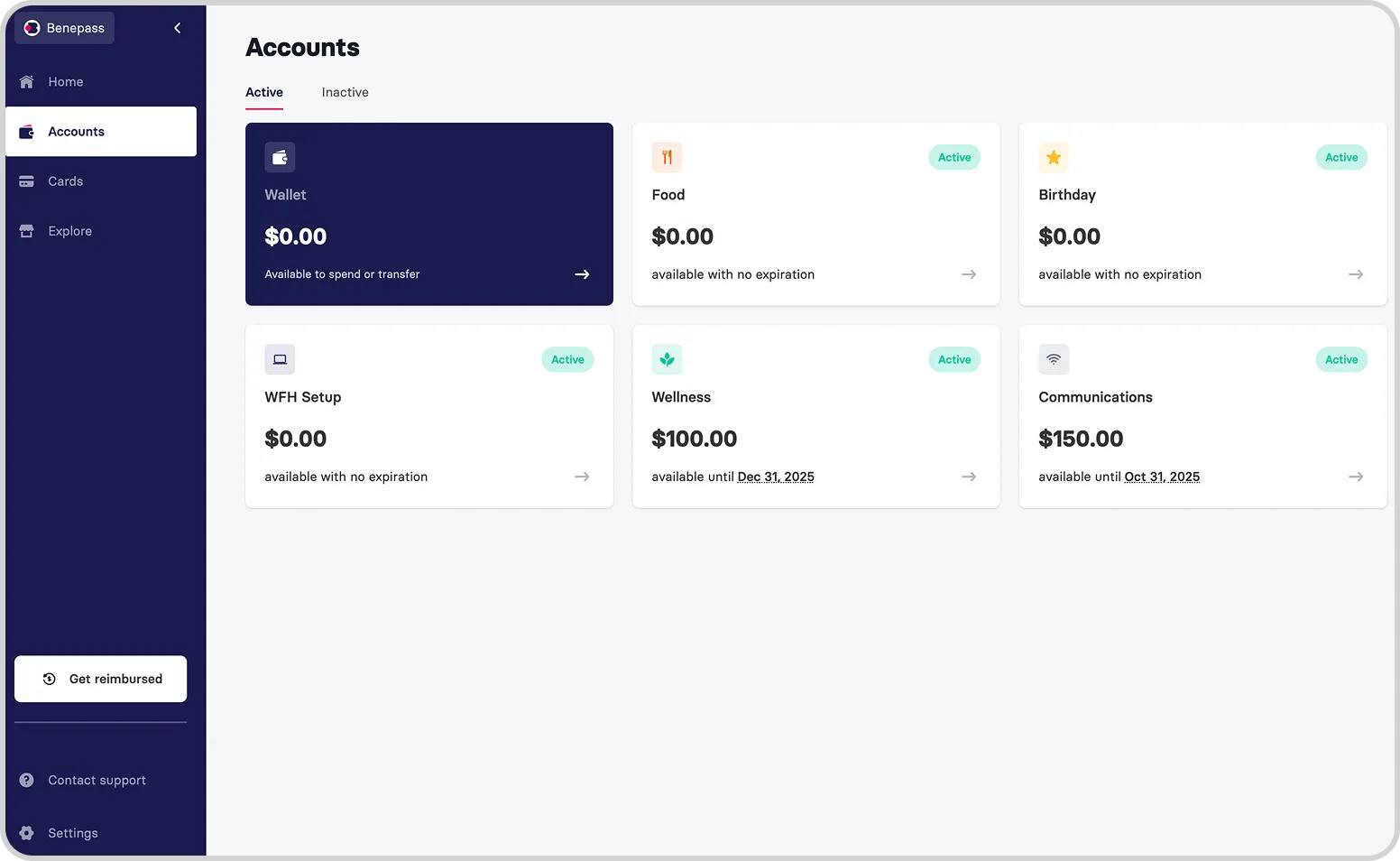

A lifestyle spending account is a fixed employer contribution that employees can spend within categories you define. Unlike traditional benefits that lock employees into specific vendors or narrow programs, LSAs let you build something that reflects your workforce's actual priorities—whether that's gym memberships, mental health support, childcare, professional development, or home office equipment.

You control the core parameters: contribution amount, eligible categories, funding frequency, and expiration rules. Most employers fund LSAs monthly or annually, with funds typically treated as post-tax income when spent. You can design a broad program that covers multiple lifestyle pillars, or focus on a single area, such as physical health or family support.

How LSA funding works

Employers contribute a fixed amount per employee on a recurring schedule. The most common structure is monthly funding with a "use it or lose it" expiration at month's end, which helps control costs since not every employee will spend their full allocation. Other companies prefer quarterly or annual cycles, sometimes with rollover so employees can save for larger purchases.

According to the 2026 Benepass Benchmarking Report:

- Out of companies offering LSAs, 63% provide a broad, multi-category program, with a median annual contribution of $1,200 per employee.

- Contribution levels vary by size and industry: small companies (300 or fewer employees) typically contribute $1,200 for broad LSA annually, mid-sized companies (300–999 employees) around $600, and large companies (1,000 or more employees) approximately $1,200.

- The most common types of LSAs employers offer include broad LSA (63% of employers), fitness and wellness (29%), work-from-home (23%), and professional enrichment (22%).

Your budget and these benchmarks are the two largest factors in setting your contribution amount. Monthly expiration drives consistent engagement and predictable costs, while annual rollover gives employees more purchasing power but requires more budget flexibility.

Benefits of lifestyle spending accounts

LSAs address several strategic priorities simultaneously, making them among the more cost-effective additions to a modern benefits package.

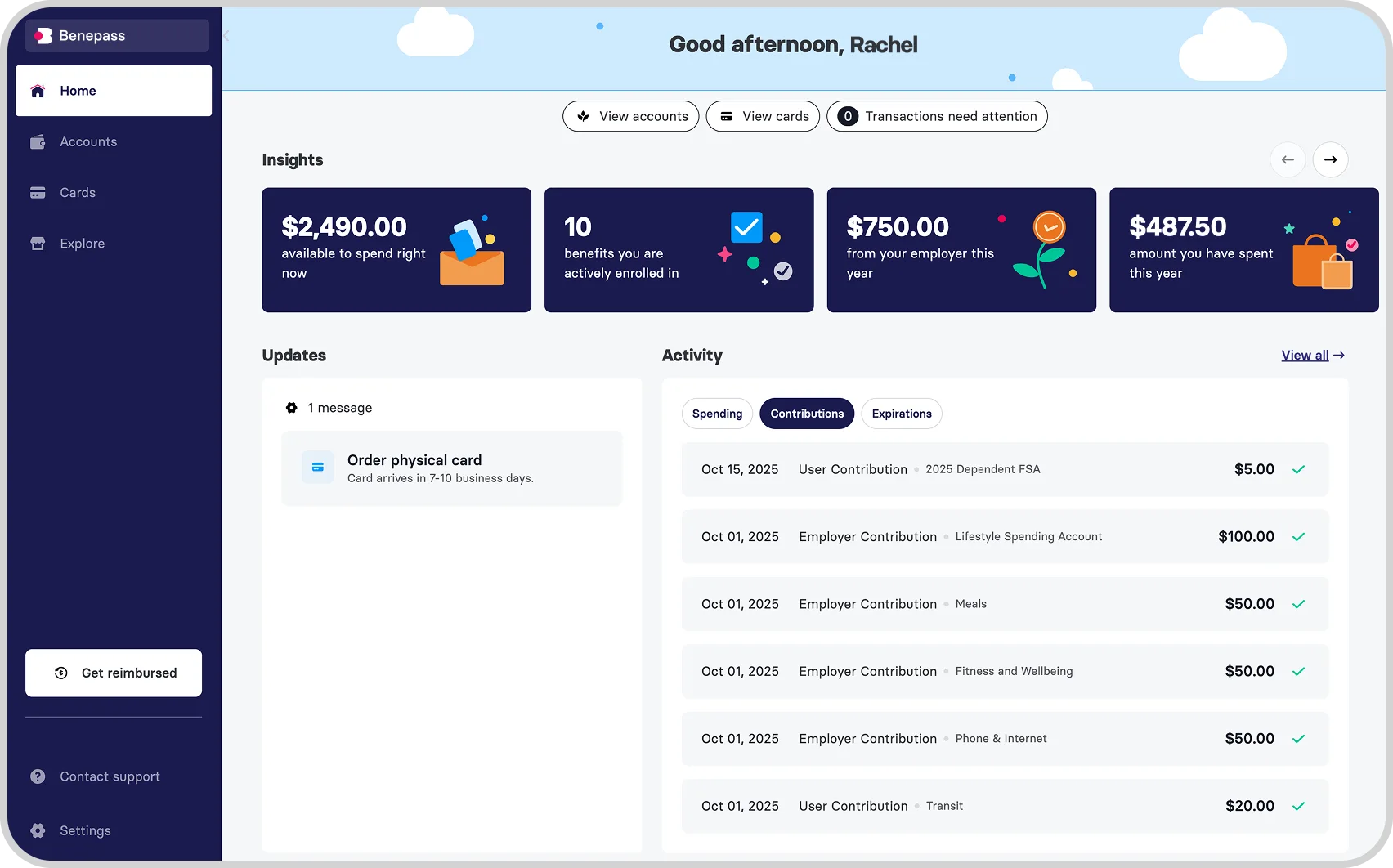

For employees, the primary advantage is flexibility. Rather than being locked into a single wellness vendor, employees can direct funds toward what actually matters to them. Employees also benefit from immediate access to funds, particularly with card-first platforms that eliminate the need to submit receipts and wait for reimbursement.

For employers, LSAs support recruitment and retention while giving you meaningful control over program costs. Organizations that embed well-being into their culture see employee retention rates improve by 10%, according to the Global Wellness Institute. LSAs also work well for distributed and global teams since employees can spend on services available in their location.

Card-first LSAs remove a real access barrier: employees don't need to pay out of pocket before reimbursement, making the benefit more accessible across income levels. Consolidating multiple point solutions into a single LSA also reduces vendor management overhead, while expiration controls keep your budget predictable.

For more on measuring return on investment, see our guide on calculating LSA ROI.

What are the challenges of lifestyle spending accounts?

LSAs are flexible and generally well-received, but a few implementation challenges are worth planning for before you launch.

LSA challenges for employees

Understanding tax implications: Most LSAs are taxable, so employees may see an impact on their take-home pay when they spend. Clear communication about how LSA spending affects paychecks prevents surprises and builds trust.

Keeping track of deadlines: Employees who miss expiration dates lose funds they could have used. Timely reminders significantly reduce this friction.

Knowing what's eligible: Without clear guidance, employees may assume certain purchases are covered when they're not. A straightforward list of LSA-eligible expenses reduces confusion and improves satisfaction.

LSA challenges for employers

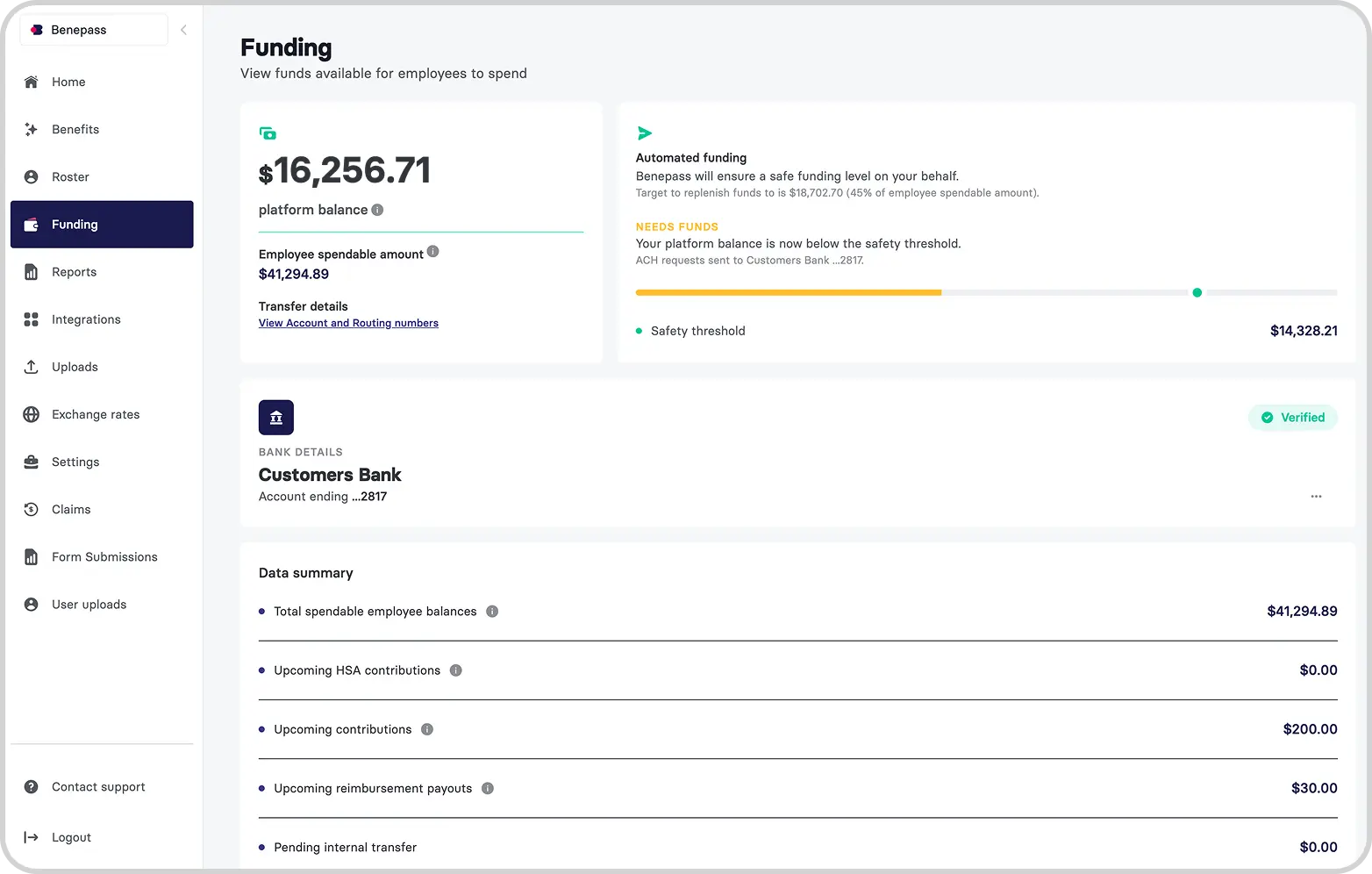

Tax management: Properly categorizing and reporting taxable LSA spending requires coordination between your benefits platform and payroll system. A provider that handles tax reporting automatically reduces the compliance burden on your HR and finance teams.

Administrative overhead: Without automation, managing reimbursements and eligibility rules can become time-consuming. The right platform handles approvals in real time and minimizes manual work, reducing the risk of errors.

Budget predictability: Usage can vary month to month, especially early in a program. Detailed reporting and expiration controls help you track spending patterns and plan more accurately over time.

These challenges are manageable with the right technology and communication strategy. Most HR leaders find that addressing them up front leads to a smooth program and strong employee engagement.

What can LSAs be used for?

LSAs are fully customizable, so you can design your program around specific employee needs. Common spending categories include:

- Physical fitness: Gym memberships, workout apps, fitness equipment, yoga classes, personal training

- Home office equipment: Desks, chairs, monitors, keyboards, cell phone and internet service

- Mental health: Meditation apps, online therapy, massage therapy, stress management programs

- Professional development: Online courses, certifications, industry conferences, continuing education

- Family support: Childcare, kids' activities, pet care, elder care services

- Personal development: Language learning, music lessons, creative workshops

- Grocery and meal delivery: Healthy meal kits, grocery delivery, nutritional supplements

- Student debt repayment: Monthly contributions toward student loan balances

- Commuter benefits: Transit passes, parking, rideshare services, fuel costs

An employee benefits survey can help you identify which categories will drive the highest engagement before you finalize your program design.

Are LSAs taxable?

LSAs are generally a taxable benefit. Employees pay taxes only on what they spend, not on the full amount allocated. However, there are exceptions. Some categories may be non-taxable if they meet IRS criteria, including:

- Work-from-home equipment

- Cell phone and internet used for business purposes

- Certain professional development expenses

To qualify, these expenses must be business-related and properly documented.

It’s best to avoid mixing taxable and non-taxable categories in one account, as it complicates reporting and increases the risk of IRS issues. Be sure to use separate accounts or wallets for each.

Your payroll system must also report LSA spending as taxable income on employees’ W-2 forms. Platforms that handle tax reporting automatically can reduce administrative work and minimize errors.

Disclaimer: Benepass offers insights based on common industry practices but does not provide tax advice. Please defer to your internal tax counsel to confirm the appropriate tax treatment for your specific programs.

LSA vs. other employee benefits: Making the right choice

Understanding how LSAs compare to other account-based benefits helps you position them correctly within your overall benefits strategy.

Lifestyle spending accounts vs. health savings accounts

An HSA is a tax-advantaged account available only to employees enrolled in a high-deductible health plan (HDHP), designed specifically for qualified medical expenses. For 2026, the IRS has stated that an HDHP requires a minimum deductible of either:

- $1,700 for individual coverage

- $3,400 for family coverage

HSAs offer triple tax advantages: contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

But LSAs have no eligibility restrictions tied to health plan enrollment, and any employee can participate regardless of which health plan they've selected. Again, LSA funds are post-tax, so employees pay income tax on what they spend.

For most organizations, this isn't an either-or decision. Offering both lets you support employees with HDHPs in managing healthcare costs while providing flexible wellness support to your entire workforce.

LSAs vs. flexible spending accounts

Flexible spending accounts (FSAs) allow employees to set aside pre-tax dollars for qualified medical or dependent care expenses. Like HSAs, FSAs:

- Are IRS-regulated

- Have specific expense categories

- Carry annual contribution limits

- Typically have stricter "use it or lose it" rules

LSAs don't carry IRS contribution limits and aren't restricted to medical or dependent care expenses, making them a better fit when your goal is broad lifestyle support. FSAs and LSAs can coexist in a benefits package, each serving a distinct purpose.

LSAs vs. traditional wellness programs

Traditional wellness programs typically involve a fixed set of vendor partnerships that all employees receive, regardless of whether they use them.

LSAs shift that model for greater flexibility and unique benefits:

- Gives employees a budget to spend on what they personally value

- Drives higher utilization because employees are choosing their own benefits

- Reduces the administrative overhead of managing multiple vendor contracts

For HR teams supporting global or distributed workforces, LSAs are particularly practical since employees can spend on services available in their location.

How to set up an LSA

Setting up an LSA is more straightforward than implementing tax-advantaged accounts, but it still requires deliberate planning.

Step 1: Set your budget. Determine how much you can allocate per employee and how often you'll fund the account. Use benchmarking data to ensure your contribution is competitive for your industry and company size.

Step 2: Define eligible categories. Survey your employees before finalizing categories. Broader programs tend to drive higher engagement because they serve more of your workforce's diverse needs.

Step 3: Select a benefits platform. Look for a vendor that offers card-first access, real-time expense tracking, automated eligibility verification, and accurate tax reporting. Evaluate vendors on how well they support custom spending categories, flexible expiration rules, and employee communication tools. For a detailed comparison, see our guide to LSA vendors.

Step 4: Communicate clearly. Employees need to understand what's covered, how to access funds, what happens to unused balances, and how LSA spending affects their taxes. Use multiple channels, including email, benefits portal, and team meetings, to ensure the message reaches everyone.

Step 5: Review and refine. Plan to revisit your program at least once a year. Track participation rates, average spend per employee, popular spending categories, and employee satisfaction scores. Use that data to adjust contribution amounts, add categories, or modify expiration rules.

Getting started with lifestyle spending accounts

If you’re considering whether an LSA fits into your benefits strategy, start with what you’re trying to solve. For many teams, it comes down to the same issues: low engagement, too many vendors, or benefits that don’t reflect how employees actually live and work.

From there, the key decisions are practical. Set a contribution level that aligns with your budget, define categories that match your workforce, and choose a structure that encourages employees to use funds consistently throughout the year. The most effective programs are shaped by how employees actually use them.

Modern platforms like Benepass are designed to ease LSA management, with configurable spending categories, card-based access, and built-in tax handling. If you’re exploring how LSAs could work for your organization, learn how Benepass LSAs can benefit your business.

Frequently asked questions about lifestyle spending accounts

What is the difference between a lifestyle spending account and an HSA?

An LSA is an employer-funded benefit employees can use across a wide range of wellness and lifestyle expenses. An HSA, by contrast, is a tax-advantaged account limited to qualified medical expenses and available only to employees enrolled in a high-deductible health plan.

LSAs are funded by employers using post-tax dollars, while HSAs can be funded by both employers and employees and offer tax advantages. LSAs provide more flexibility in how funds can be used, but they don’t carry the same tax benefits as HSAs.

Is a lifestyle spending account taxable?

Yes, LSAs are generally taxable. When employees spend LSA funds, those amounts are treated as taxable income at the federal, state, and local levels. Employees pay taxes only on what they spend, and funds forfeited are not taxed.

Some categories may qualify for non-taxable treatment, such as work-related equipment or professional development, but they must meet specific IRS criteria. Always defer to your internal tax counsel to confirm the appropriate tax treatment for your specific programs.

What are the pros and cons of lifestyle spending accounts?

The main advantages of LSAs are flexibility, cost control, and simpler administration. They give employees more choice in how they use benefits, help attract and retain talent, and can replace multiple point-solution vendors with a single program. Expiration policies also give employers more predictable budget control.

The trade-offs are straightforward. LSA funds are typically taxable, setup requires decisions around categories and contribution levels, and employees need clear communication to use the benefit effectively.

How much should companies contribute to LSAs?

Benchmark against similar organizations in your industry and size category. According to the 2026 Benepass Benchmarking Report, small companies (300 or fewer employees) contribute a median of $1,200 annually to broad LSA, mid-sized companies (300–999 employees) around $600, and large companies (1,000 or more employees) approximately $1,200.

However, on the industry front, tech companies contribute a median of $775 annually to broad LSA, while healthcare and biotech service companies contribute a median of $1,200 annually.

Can LSA funds roll over to the next year?

Yes, funds can roll over to the next year. Some employers use a "use it or lose it" model with monthly or annual expiration, which controls costs and encourages regular engagement. Others allow annual or indefinite rollover, giving employees flexibility to save for larger purchases. Your benefits platform should support whichever structure you choose and communicate expiration timelines clearly to employees.

Frequently Asked Questions

Rebecca Noori

Rebecca Noori is a freelance HR Tech and SaaS writer who is obsessed with our world of work. She writes about everything from employee benefits and performance management to upskilling and productivity tips. When she's not writing, you'll find her grappling with phonics homework and football kits, looking after her three kids.

.jpg)