In this post

Lorem ipsum dolor sit amet

Lorem ipsum dolor sit amet

The IRS released the 2027 health savings account (HSA) and high-deductible health plan (HDHP) limits on May 29, 2026, giving benefits teams a long runway to update plan materials before open enrollment. Now is the time to take advantage of that head start.

This go-to reference covers what changed, when each figure takes effect, and what HR has to do about it.

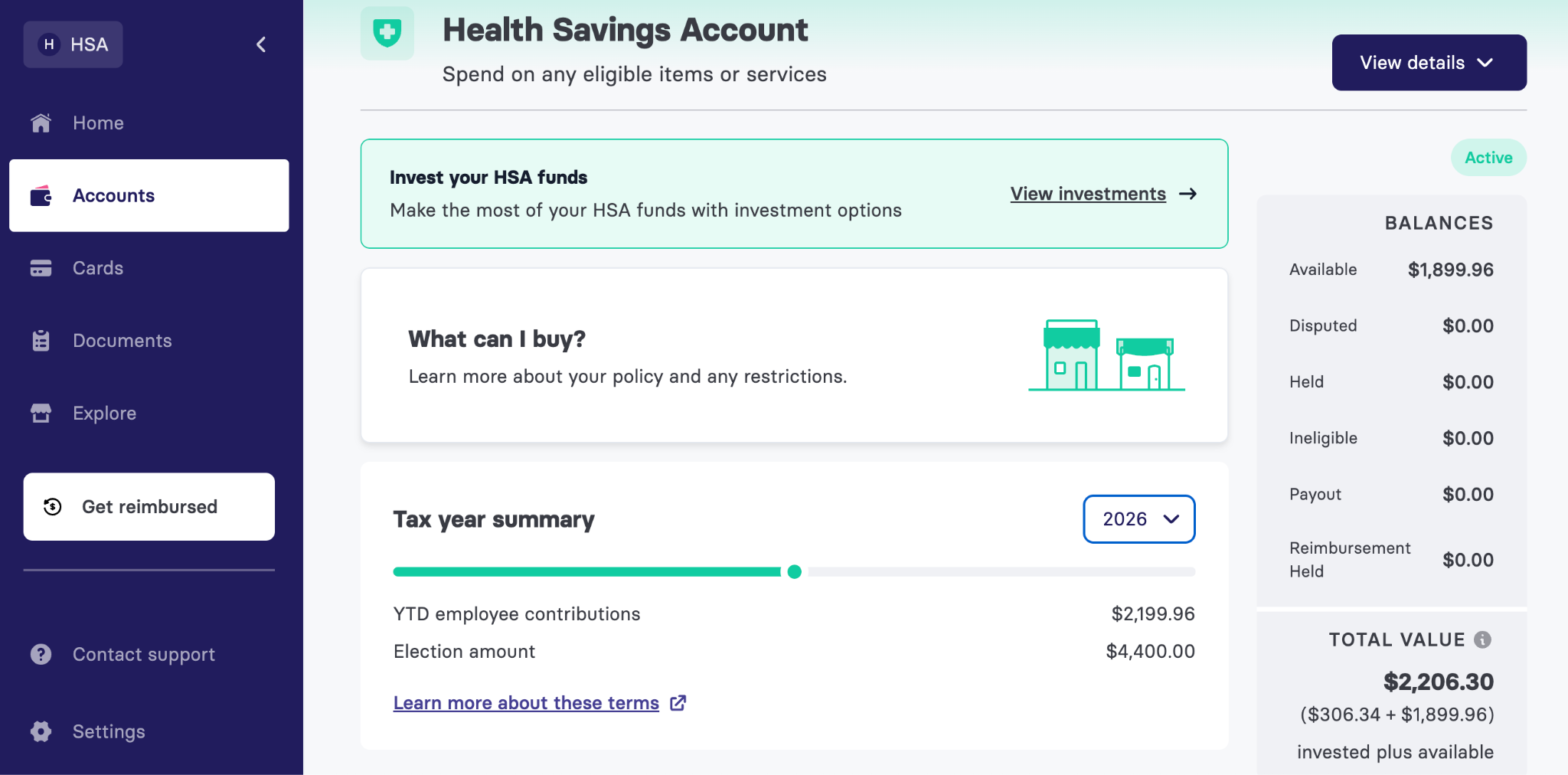

What are the 2027 HSA contribution limits?

For 2027, referencing the IRS Revenue Procedure 2026-24, there were a couple changes to the HSA contributions:

- $4,500 for self-only coverage, up $100 from $4,400 in 2026

- $9,000 for family coverage, up $250 from $8,750

Account holders who are 55 or older by the end of the tax year can add a catch-up contribution of $1,000, which is a fixed amount set by statute and not adjusted for inflation, so it stays flat year over year.

One detail that often trips up employees is the annual limit is an aggregate cap. It covers everything that goes into the account from every source, including employee payroll deductions, employer seed contributions, and wellness incentives. If your company contributes $1,000 to an employee's family HSA in 2027, that employee can contribute $8,000 of their own money before hitting the $9,000 ceiling.

2027 HDHP and out-of-pocket limits

An HSA is only available to employees enrolled in a qualifying high-deductible health plan, so the HDHP thresholds matter as much as the contribution limits. A plan that falls outside these figures is not HSA-eligible, and employees enrolled in it cannot contribute. Both the minimum deductible and the out-of-pocket maximum moved up for 2027.

Minimum deductible requirements

To qualify as an HDHP in 2027, a plan must carry an annual deductible of at least $1,750 for self-only coverage, up from $1,700 in 2026, or $3,500 for family coverage, up from $3,400, per IRS Revenue Procedure 2026-24. A plan with a deductible below these figures does not meet the definition, which means anyone enrolled in it loses HSA eligibility for the year. Confirm your 2027 plan designs clear these minimums before you publish enrollment materials.

Out-of-pocket maximums

The maximum out-of-pocket for a qualifying HDHP cannot exceed $8,700 for self-only coverage in 2027, up from $8,500, or $17,400 for family coverage, up from $17,000. These ceilings include deductibles, copayments, and other cost-sharing, but they exclude premiums. A point worth raising in plan design conversations is that the HDHP out-of-pocket maximum is separate from, and lower than, the ACA out-of-pocket maximum for non-grandfathered group plans, which CMS set at $12,000 self-only and $24,000 for other coverage in 2027.

2027 limits at a glance: 2026 vs. 2027 comparison

For convenience, this table is built to copy and paste directly into benefit guides, enrollment portals, and employee communications, and every figure traces to IRS Revenue Procedure 2026-24.

The excepted-benefit health reimbursement arrangement (HRA) limit, separate from the HSA limit, applies to plan years beginning in 2027 and rises to $2,250 from $2,200.

When do the new limits take effect?

The 2027 limits are effective January 1, 2027 for calendar-year plans, which covers most employers. For non-calendar-year plans, figures correspond to their plan year, so a plan year that begins in mid-2027 follows the 2027 HSA contribution limits for that year.

So if your medical plan runs on a fiscal or off-cycle year, confirm the effective date with your administrator before you communicate any numbers—because applying the wrong year's limit to payroll elections creates correction work later.

What hasn't changed: FSA limits and the fall release

FSAs operate differently from HSAs, and the 2027 flexible spending account (FSA) and dependent care FSA limits are not published yet. The IRS releases HSA figures in the spring, ahead of FSA and 401(k) limits, which typically arrive in the fall. Do not assume, carry forward, or communicate a 2027 FSA number until the IRS releases it. Telling employees a figure that later changes leads to re-issuing materials and walking back guidance during the busiest stretch of the year.

The distinction between HSA and FSA rules also confuses employees during enrollment, so reinforce while you have their attention:

- HSA balances roll over in full year after year and the account belongs to the employee for life, even after they leave the company.

- Most FSAs operate on a use-it-or-lose-it basis, with only a limited carryover or grace period if the plan allows one.

What employers should do before open enrollment

The early release is the advantage. Here is how to use the runway so the 2027 changes land cleanly instead of becoming a scramble in the fall.

- Update every place the numbers live. Benefit guides, enrollment portals, plan documents, and payroll deduction caps all need the new HSA, HDHP, and excepted-benefit HRA figures.

- Confirm your HDHP designs still qualify. Check each plan's deductible against the $1,750 and $3,500 minimums and its out-of-pocket maximum against the $8,700 and $17,400 ceilings. A plan that drifts outside that range costs employees their HSA eligibility.

- Coordinate with payroll. Make sure pre-tax election maximums reflect the new limits so employees can contribute the full amount without tripping a system cap and so contributions don’t exceed the aggregate limit.

- Brief the team that fields questions. Whoever answers benefits questions should know the new figures, the aggregate-cap rule, and the fact that 2027 FSA limits are not out yet, so employees get a consistent answer.

Rising healthcare costs make this prep more consequential than it used to be. The 2026 Benepass Benefits Benchmarking Report found that 51% of employers exceeded their healthcare budgets in 2026, and as more cost shifts to employees through higher deductibles, reliance on HSAs and FSAs keeps climbing.

The teams that struggle each year are usually the ones updating the same limit in several disconnected vendor portals by hand. Running HSAs, FSAs, HRAs, and other pre-tax accounts on one platform ensures a limit change gets pushed across every program at once instead of being re-keyed vendor by vendor.

Help employees actually use the higher limits

Raising a contribution limit only matters if employees contribute and spend. Most employers face a participation and education gap, not a generosity gap, and a higher ceiling does nothing on its own to close it. The fix is making the account easy to understand and easy to use.

That is where consolidation and a card-first experience earn their keep. The 2026 Benepass Benefits Benchmarking Report found that 37% of Benepass clients running both pre-tax and lifestyle accounts on a single platform see higher FSA utilization, at 85% versus 79% for employers running fragmented programs. Card-first behavior tracks the same way: HSA utilization reaches 91% when employees can swipe a card instead of filing claims. When the account is visible and the spending is frictionless, employees treat the higher limit as something they can actually act on.

Pairing updated limits with employee education on pre-tax benefits and a single card and account experience gives employees a clear way to track contributions and spend down balances.

Plan for 2027 with limits you can act on

The annual limit update reads like a compliance checkbox, but it's really a yearly stress test of your benefits stack. Can it absorb a change like this without a manual scramble across vendor portals? Can employees see and use the higher limits without a separate explainer for every account? The employers who answer yes are the ones who consolidated pre-tax administration before the figures dropped, not the ones reacting to them now.

What HR actually wants out of this is straightforward: a benefits program that stays compliant and well-used without piling on admin work every January. The 2027 numbers are an early, concrete chance to build toward that, while there’s still time before open enrollment to get it right.

Push the new 2027 limits across your HSA, FSA, and HRA programs from one platform, like Benepass, and give employees a single card and account experience that makes higher contributions easy to track and use.

To learn more about how Benepass can bring pre-tax accounts together, schedule a demo with our team.

Frequently asked questions

Do employer contributions count toward the 2027 HSA limit?

Employer contributions do count toward the HSA limit. The HSA contribution limit is an aggregate cap that includes money from every source: employee payroll deductions, employer seed contributions, and wellness incentives all count toward the same ceiling. For 2027, that ceiling is $4,500 for self-only coverage and $9,000 for family coverage. If an employer contributes $1,000 to a family HSA, the employee can add up to $8,000 of their own money before reaching the limit.

Can employees age 55 and older contribute more in 2027?

Employees who are 55 or older by the end of the tax year can make a catch-up contribution of $1,000 on top of the standard limit, bringing their 2027 maximum to $5,500 for self-only coverage or $10,000 for family coverage. The catch-up amount is fixed by statute and does not change with inflation. If both spouses are 55 or older, each must use a separate HSA to claim their own catch-up.

When will the 2027 FSA contribution limits be announced?

The 2027 FSA and dependent care FSA limits have not been released yet. The IRS publishes HSA figures in the spring but typically releases FSA and 401(k) limits in the fall. Until the official figures are out, employers should not assume or communicate a 2027 FSA number, since publishing a figure that later changes means re-issuing materials during enrollment season.

Frequently Asked Questions