In this post

Lorem ipsum dolor sit amet

Lorem ipsum dolor sit amet

Every HR leader designing a benefits program works inside a squeeze. Leadership wants costs controlled and predictable. Employees want benefits that fit their actual lives, which rarely look the same across a workforce that spans early-career hires, parents, and people planning for retirement. Those two pressures almost never point in the same direction, and the employee benefits program is where they have to be reconciled to attract and retain talent.

A well-designed program is how you do that. It should fit the budget you can defend to finance, stay compliant with federal and state requirements, and appeal to the people it's meant to serve. This guide walks through the design process step by step, so you can build a program that holds up year over year instead of one you rebuild every open enrollment.

What makes an employee benefits program effective?

An employee benefits program is the full set of compensation an employer provides beyond salary, spanning legal requirements, core health and retirement plans, and flexible or supplemental options. The required pieces are non-negotiable. The choices you make beyond them are where design actually happens.

A strong program tends to share four markers:

- Clear goals. Every benefit ties to an outcome the business cares about, like employee retention, recruitment, or cost control, rather than sitting in the lineup because it always has.

- Real utilization. Employees know what they have, understand it, and use it. A benefit no one touches is budget spent without return.

- Cost control. Spend stays aligned with workforce value, and you can model what happens when enrollment or claims shift.

- Compliance. The program meets IRS, ERISA, ACA, and applicable state requirements, with documentation you can produce on request.

The thread connecting all four is flexibility. A single workforce holds wildly different priorities at once, and a rigid program forces everyone into the same set of choices. Flexible options let one program serve a 25-year-old paying down student loans and a 50-year-old maximizing retirement contributions without designing two separate plans.

That range is increasingly what employees expect. According to the 2026 Benepass Benefits Benchmarking Report, 39% of employers are now expanding income-supplement benefits covering essentials like food, commuting, and housing, a sign that targeted, flexible support has moved into the core of how companies think about total rewards.

How to design an employee benefits program step by step

Designing a program is a sequence, not a single decision. Each step builds on the one before it, and skipping ahead, like picking vendors before you understand your workforce, is where most programs go wrong, and note that consolidating pre-tax, lifestyle, and wellness benefits onto one platform reduces the administrative burden that fragments many programs.

1. Set program goals and a realistic budget

Start with the outcomes the program needs to deliver. Name them specifically:

- Cut voluntary turnover by a set percentage

- Stay competitive for a hard-to-fill role

- Hold benefits spend within a defined ceiling

Vague business goals like "improve morale" give you nothing to measure against later.

Then ground the budget in data. Benefits typically run 30% of total compensation, as reported by the U.S. Bureau of Labor Statistics. So the number you commit to shapes every choice that follows. Model a few scenarios before you lock anything in: What happens to cost if enrollment rises 15% or if you shift health plan structures? Finance and HR should build these projections together because a budget set without modeling is a guess, and guesses get expensive at scale.

2. Understand your workforce and gather employee input

A program built on assumptions serves no one well. Collect data before you design:

- Run anonymous employee benefits surveys to surface what employees actually value and where they feel unsupported, asking direct questions like which benefits matter most and what would make them feel more secure.

- Review existing benefits data for participation patterns. Low uptake on a 401(k) or health savings account (HSA) often signals cash flow pressure to address first.

- Segment by life stage and demographics, as financial priorities vary sharply between early-career employees, parents, and those nearing retirement.

This input does two things: it tells you where to spend, and it gives you a baseline to measure against once the program launches.

3. Choose your core and supplemental benefits mix

With goals and workforce data in hand, build the actual package. Most programs layer three tiers:

- Core benefits like medical coverage, dental or vision insurance, life insurance, and disability coverage, plus retirement benefits, form the foundation employees expect.

- Pre-tax accounts such as HSAs, FSAs, HRAs, and commuter benefits stretch employee dollars and lower payroll tax costs for the company.

- Supplemental and lifestyle options like wellness programs, professional development funds, and family care support cover the needs that don't fit a standard category.

The supplemental tier is where flexibility pays off, and it often costs less than core benefits while carrying strong retention impact. This is also where the case for consolidation starts. Employees engage more with their benefits when the experience is consistent, and offering flexible and pre-tax options through one system rather than scattered vendors makes that possible.

4. Confirm compliance and required benefits

Some benefits are mandatory, and the design work here is about getting the requirements right, not choosing among options. At the federal level, employers must provide Social Security, Medicare, unemployment insurance, and workers' compensation. Employers with 50 or more full-time employees face additional obligations under the Affordable Care Act, which requires affordable health coverage under the IRS employer shared responsibility provisions, and the Family and Medical Leave Act, which mandates up to 12 weeks of job-protected leave.

State requirements layer on top and vary widely. Several states mandate paid family leave, disability insurance, or specific unemployment contributions that go beyond federal rules. Build a compliance calendar, run an annual plan review, and consider involving benefits counsel—because a single missed notice or incorrect plan document can trigger meaningful penalties.

5. Select vendors and check HRIS and payroll integration

Vendor selection is where many programs quietly accumulate cost and complexity. Each new point solution adds another login, another file feed, and another vendor relationship for your team to manage, and that fragmentation is exactly what drives up administrative time.

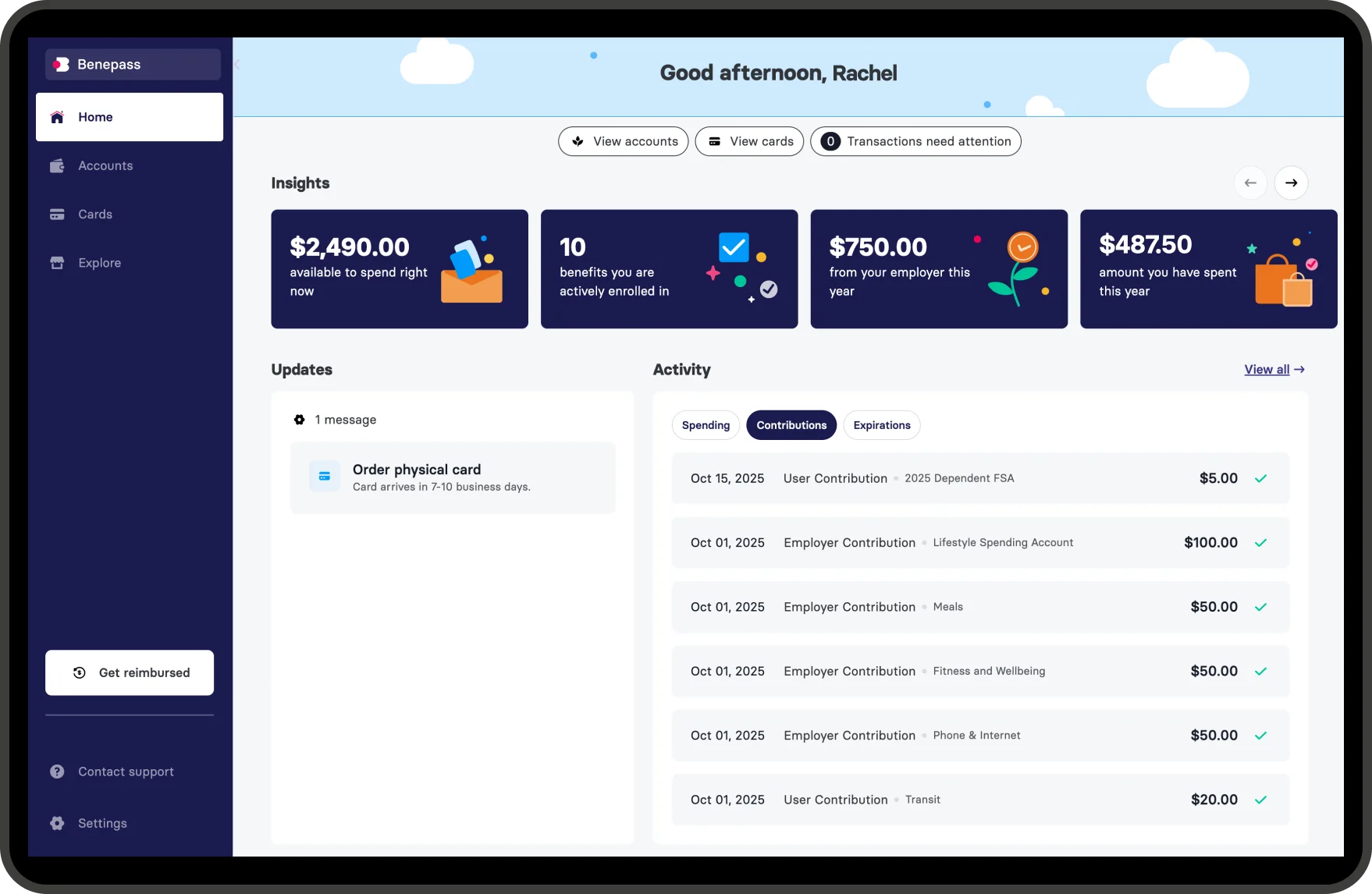

Consolidating pre-tax, lifestyle, and wellness benefits onto a single platform reduces that burden. It also improves the employee experience, which in turn lifts utilization. The 2026 Benepass Benefits Benchmarking Report found that employers running flexible spending accounts (FSAs) alongside an lifestyle spending account (LSA) on one platform see 85% FSA utilization, compared to 79% for employers with fragmented programs. When employees engage with one flexible account, they pay more attention to the rest of their benefits and leave fewer dollars unspent.

Whatever you choose, confirm it connects to your existing systems. A platform that automates enrollment, contributions, and deductions through HRIS and payroll integrations removes manual data entry and the reconciliation errors that come with it.

6. Plan rollout, open enrollment, and communication

A strong program still fails if employees don't understand it. Roll out in phases when you can, starting with a pilot group across different teams so you can catch friction before a company-wide launch.

Communication carries the most weight here, and it can't be a single email at open enrollment. Focus your messaging on outcomes employees care about, like paying down debt or covering childcare, rather than generic plan descriptions. Use the channels you already have, including team meetings, newsletters, and manager toolkits, and keep visibility going year-round with reminders tied to moments like tax season. Consistent communication is what turns a well-designed program into a well-used one.

7. Measure utilization and refine over time

Set baseline metrics before launch, then track them on a regular cycle rather than waiting for renewal. Watch three categories:

- Participation and enrollment rates

- Utilization across each benefit type

- Business outcomes like voluntary turnover and time-to-fill

Review results quarterly. Low utilization on a specific benefit is a signal, telling you to communicate it differently, replace it, or redirect that budget toward something employees actually use. Programs that improve continuously outperform set-and-forget plans by a wide margin over a three-to-five-year horizon and positively contributes to company culture. Plus, the data you collect is also what lets you defend the budget and expand what's working.

Common mistakes to avoid when designing a benefits program

Even careful benefits administration runs into the same recurring problems. Watch for these:

- Offering benefits no one uses. Benefit plans that are added because a competitor has them, without checking workforce data, become budget spent for no return. Let employee input drive the mix.

- Under-communicating at enrollment. A program employees don't understand is one they won't use or value. Invest in communication year-round, not just during the enrollment window to maintain steady employee engagement.

- Ignoring workforce data. Designing on assumptions instead of survey results and participation patterns produces a program that fits no one in particular and lowers employee satisfaction.

- Letting vendor sprawl drive up cost. Each disconnected point solution adds admin time and another bill. Consolidation keeps both in check.

A benefits program is never finished

The strongest programs treat design as an ongoing loop rather than a once-a-year setup. You measure, you learn what's working, and you adjust. When workforces shift, costs move, and the priorities of your people change with them. A program that looked right two years ago can quietly drift out of step with what your team needs today, and the only way to catch that is to keep watching the data.

That ongoing work is far easier when you aren't fighting your own tooling to do it. Benepass gives HR teams one configurable platform to fund, administer, and adjust pre-tax, lifestyle, and wellness benefits, with the employee experience and reporting you need to see what's being used and act on it. Instead of reconciling vendors, you spend your time on the design decisions that actually move retention and engagement.

Explore how Benepass helps HR teams design, fund, and adjust a flexible benefits program from one configurable platform built for modern workforces.

Frequently asked questions

How much should a company budget for an employee benefits program?

Benefits typically cost around 30% of total compensation, but the right number for your company depends on headcount, industry, and the benefits mix you choose. Rather than starting from a fixed figure, model a few scenarios with finance to see how cost shifts with enrollment and plan design changes, then set a ceiling leadership can defend.

What benefits are legally required for employers?

At the federal level, employers must provide Social Security, Medicare, unemployment insurance, and workers' compensation. Employers with 50 or more full-time employees must also offer affordable health insurance under the Affordable Care Act and up to 12 weeks of job-protected unpaid leave under the Family and Medical Leave Act.

States layer on additional requirements, and several mandate paid family leave or disability insurance, so confirm your obligations in every state where you employ people.

How often should you review and update a benefits program?

Review utilization, claims, and employee feedback quarterly rather than waiting for the annual renewal, which lets you catch issues before they compound. Plan a deeper design review every one to two years, or whenever your workforce changes significantly through growth, a shift in demographics, or expansion into new locations. Treat review as continuous to keep the program aligned with what employees need and what the budget can support.

Frequently Asked Questions